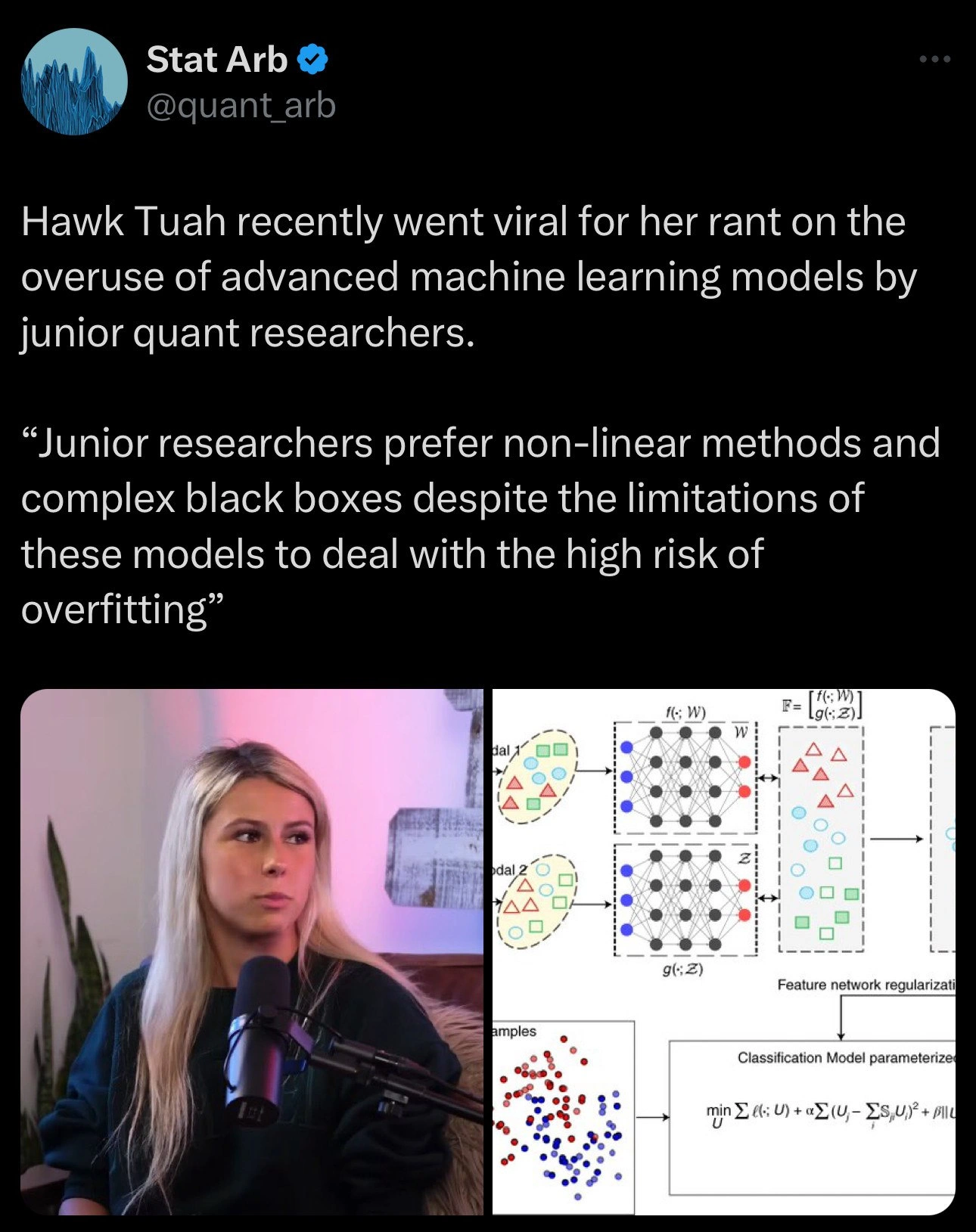

Hawk Tuah's Unlikely Pivot to Critiquing Overfitting in Quant ML Models

Why is this AI ML meme funny?

Level 1: Rocket to the Store

Imagine a kid who just got a shiny new toy rocket. She’s super excited and says, “Let’s use this rocket to go to the store down the street!” She thinks the rocket is the coolest, fastest way to travel because, well, rockets are awesome and advanced. Now, the parent looks at her and remembers that the store is literally a few blocks away. The parent suggests, “How about we just ride a bike or walk? That rocket is a bit overkill, and it might even blow up or go off course.” The kid is dazzled by the fancy rocket (it’s new! it’s complex! it promises an exciting ride), so she’s ignoring the simple, reliable solution right in front of her.

This meme is just like that story. The junior researchers are like the excited kids with the new rocket – they’ve got these super fancy AI models (the rocket) and want to use them for everything, thinking it’ll surely be the best. The senior researchers are like the parents – they know that sometimes the “big fancy rocket” approach is unnecessary and even risky when a regular solution (the bike or just walking) would work better. It’s funny because we understand the kid’s enthusiasm, but we also see the silliness: you don’t need a rocket to visit a nearby store, and in fact, that could end in disaster (imagine a rocket trying to land by the grocery – not good!). In the same way, you don’t always need an ultra-complicated model to solve a problem; sometimes a simple one is safer and gets the job done without fuss.

So the humor and the heart of this meme is about over-complicating things. It’s showing us that sometimes people new to a field get so caught up in the latest cool thing that they forget the basics. Just like a child might choose the flashiest tool for a simple task (“I’ll use a rocket to deliver this pizza!”), junior folks in tech might choose a super advanced algorithm for a straightforward problem. And just like a wise parent chuckles and guides the kid to a saner option, the experienced engineers kind of smile, shake their heads, and try to steer the juniors back to a simpler, more sensible solution. It’s a gentle life lesson: fancier isn’t always better, and often the simplest solution is the one that works best in real life.

Level 2: Bigger != Better

Let’s break down the technical jargon and context of this meme in simpler terms. The setting here is quant finance – that’s the world of quantitative trading and research, where math, programming, and finance meet. A quant researcher is basically a scientist of finance who uses models and data to predict market moves or find trading opportunities. Now, what’s happening is that some junior (less experienced) people in this field are very excited about using advanced machine learning techniques (like complex algorithms) for their trading models. They love things like Neural Networks, which are a type of algorithm inspired by the brain that can find very complicated patterns (we call these non-linear methods because they can fit wiggles and curves in data, not just straight lines). These juniors sometimes treat these complex models as magical black boxes – “black box models” meaning you put data in, get a prediction out, but it’s hard to see or explain how it decided on that prediction because the inside is so opaque and complicated. It’s like a mystery box that does a lot of math inside; even the programmers might not fully understand what’s going on in each layer of a deep neural network when it’s making decisions.

On the other hand, there are simpler methods – like linear models (imagine a single straight line or flat plane fitting through data points). A linear model is easy to understand: it’s basically an equation where you multiply inputs by weights and add them up. For example, a linear model might predict stock returns with a formula like: return = 2*(earnings growth) + 1.5*(market momentum) - 0.5*(interest rate). Each weight (2, 1.5, -0.5) shows how important that factor is. It’s interpretable: you can see which factor matters and how. A non-linear model (like a deep neural network) could do something far more complex – it might create intermediate “hidden” features, combine inputs in weird ways, basically form a super-complicated formula with hundreds of terms. It’s powerful because it can capture nuance, but it’s also much harder to interpret or trust because you as the researcher can’t easily say why it’s making a given prediction.

Now, the big term in the tweet: overfitting. Overfitting is a fundamental concept in MachineLearning and statistics. It’s what happens when your model learns the training data too well, including the random quirks and noise, so that it fails to generalize to new data. Think of it like studying for a test: if you just memorize the answers to specific questions that were on the practice test (training data) instead of learning the underlying concepts, you’ll ace the practice test but flunk the real test if the questions change. In modeling, an overfitted model might, say, perfectly predict past stock prices (because it effectively “memorized” every twist and turn that happened historically), but when you give it tomorrow’s data, it performs poorly because those exact twists and turns aren’t repeated. It didn’t learn the true general pattern (if any); it learned the noise. Risk_of_overfitting is especially high with very complex models – they have so many adjustable parts (parameters) that they can adjust themselves to fit literally anything, including pure randomness in your dataset.

The meme specifically mocks juniors who “prefer non-linear methods and complex black boxes despite the limitations of these models to deal with the high risk of overfitting.” In plainer words, it’s saying: newbies like using super fancy complicated models even though those models often have a big weakness – they tend to overfit if you’re not very careful. The “limitations… to deal with… overfitting” means these models don’t naturally guard against overfitting; you have to apply special techniques to prevent it (otherwise they’ll happily learn nonsense patterns). One such technique is regularization. Regularization is mentioned in the meme (the right side image has a “feature network regularization” term in the diagram). Regularization is basically a fancy term for adding some constraints or penalties on a model to keep it from going wild. For example, one kind of regularization is adding a penalty in the training process for large weights – this kind of says “keep the model simpler, don’t give any one input too much crazy influence unless absolutely necessary.” Another kind is dropout (in neural nets) where you randomly drop some connections during training, forcing the network not to rely on any one memorized path. In the diagram, the formula shown suggests they penalize certain differences and the norm of weights (that $\alpha$ and $\beta$ stuff) – that’s regularization to fight overfitting.

Let’s talk about that diagram on the right: It’s basically a visualization of a neural network architecture with two branches (perhaps two types of input data, often called multi-modal because it could be like one network processing, say, news text, and another processing stock prices; “Modal 1” and “Modal 2” in the image). Those colored shapes (triangles, squares, circles) probably represent different features or data points in each modality. Each of those flows into a small neural network (the black dots might be neurons in hidden layers). Then those two come together and eventually feed into a final classification or prediction (the diagram shows them merging towards a result). The equation below shows a loss function (the thing the model tries to minimize when training). It’s got the normal part $\sum \ell(\cdot)$ which is the model’s error on training examples (how far off its predictions are), and then it has $+ \alpha (...)^2 + \beta ||...||^2$ – those are exactly the regularization terms as we discussed. So effectively, the juniors’ fancy model is so complicated that the diagram itself includes measures to mitigate overfitting. The meme is pointing out a bit of irony: these junior quants jump to super complex solutions and then have to patch them with all these extra measures (regularization, etc.) to address the very problems they invited (like overfitting) by choosing such complexity up front.

Meanwhile, the left side of the meme shows a woman (Hawk Tuah) speaking into a microphone in a podcast setting. This visual tells us that she’s publicly speaking or ranting about this issue – likely simplifying these concepts for an audience and calling out the trend. Her expression and posture say “listen up, this is important.” So, the meme combines an informal commentary medium (a podcast rant, which many people, even outside the field, might listen to) with a very formal technical illustration (an academic diagram). This contrast itself is humorous: it’s like someone holding up an overly complex blueprint while saying “See this? This is what those youngsters are doing – can you believe it?”

Now, if you’re a junior developer or data scientist, you might wonder: why not use the most powerful tool? If neural nets are so powerful, isn’t that good? The lesson here (and why seniors chuckle) is that bigger or more complicated isn’t always better. In fact, in many cases a simpler model can outperform a complex one on new data, especially if you don’t have a ton of data to train on or you haven’t done all the careful validation steps. In quant finance, data can be limited or very noisy (markets are unpredictable), so a simple approach often holds up better out-of-sample. There’s also the issue of interpretability: with a simple model, you can explain to your boss or a regulator why the model is making a certain trade (“Because interest rates went up and our model has a negative weight on that, it predicts a price drop”). With a deep neural net, if it says “buy stock A, sell stock B,” and someone asks “why?”, you often can’t easily answer – it’s a jumble of thousands of weights inside. That’s another reason seniors don’t always trust black boxes blindly, especially in fields like finance where a wild bet can lose real money.

To illustrate the core problem of overfitting in a more concrete way, consider this tiny code-like scenario:

# Junior's complex model approach (pseudo-code)

model = DeepNeuralNet(layers=50) # a deep model with 50 layers, wow!

model.fit(train_data)

print("Training accuracy:", model.score(train_data)) # say it prints 99% - excellent on known data

print("Test accuracy:", model.score(test_data)) # ouch, 55% on new data - barely better than chance

# Senior's simpler model approach (pseudo-code)

model_simple = LinearModel() # just a basic linear model

model_simple.fit(train_data)

print("Training accuracy:", model_simple.score(train_data)) # maybe 75% on training - not perfect, but decent

print("Test accuracy:", model_simple.score(test_data)) # 72% on new data - hey, it generalizes much better!

In this hypothetical code, the junior’s deep model memorized the training data (99% accuracy there) but flopped on the test data (55%, which is like random guessing if it’s a binary outcome). That’s overfitting in action. The senior’s simpler model didn’t memorize as much (75% on training) but held up on test (72%), which likely beats the deep model on what actually matters: new data performance. This is a simplified example, but it captures why just throwing complexity at a problem can backfire. The Bigger != Better mantra here is that a model should be only as complex as needed to capture the signal in the data – anything more and you’re capturing noise. When models get too complex for the problem at hand, you end up with something fragile.

In everyday terms: if you have a small dataset or a straightforward problem, using a giant deep learning model is like hiring a 100-person orchestra to play a tune that a single guitar could handle; sure, it’s powerful, but it introduces a lot of extra noise and coordination issues that might ruin the song. The meme is basically a senior person saying to juniors, “Keep it simple, don’t use a rocket ship when a bicycle will do.” Focus on understanding the data and the problem first. Use complex non_linear_methods when you truly need them and when you can control them (with things like proper testing and regularization). Otherwise, you’re just building a very elaborate castle on sand.

Let’s also decode “P&L reality” quickly: P&L stands for Profit and Loss, which is essentially how much money you’re making or losing. In quant terms, a strategy with positive P&L is good (profit!), negative is bad (loss). When they say the enthusiasm “crashes into P&L reality,” they mean that all these hyped models eventually face the real-world test: do they make money consistently or not? If a model was overfit or built on shaky assumptions, reality (P&L) will deliver a swift verdict – it won’t work and you’ll see losses. That’s the ultimate check, beyond pretty charts or high theoretical accuracy.

So, for a junior or someone newer: the takeaway is that this meme is cautionary and humorous. It defines a common pitfall: don’t worship complex AI models blindly. Always remember the basics: check for overfitting, use simpler baselines for comparison, and be skeptical of anything that’s too good to be true on historical data. It’s a gentle ribbing of those who jump on the AI hype bandwagon without the due diligence. Even though it’s cast in a quant finance scenario (with trading models and viral rants), the lesson really applies across many areas of tech. Anyone who’s seen a newbie insist on using the latest fancy framework or algorithm when a simple one would do can relate. As the meme tags suggest, this is a bit of DataScienceHumor that also illustrates the perennial Senior vs Junior developers dynamic: experience teaches you to value simplicity and robustness, whereas inexperience often overestimates the payoff of complexity.

Level 3: Black Box Overkill

From a senior quant’s perspective, this meme nails a familiar AI hype vs. reality scenario. It’s essentially data science humor portraying the tug-of-war between wide-eyed junior enthusiasts and battle-tested veterans in a quant finance setting. We have a junior researcher archetype enamored with complex black-box models – the kind who says, “Deep learning is cool, let’s use a 100-layer neural net, it’ll definitely find alpha (profit) in our data!” Meanwhile, the senior folks facepalm because they’ve seen this movie before: enormous models that claim to predict market movements flawlessly in backtests, only to flop spectacularly on real data. The tweet by “Stat Arb” (an account cleverly named after statistical arbitrage, a field that traditionally relies on rigorous statistics and often simpler linear models) highlights Hawk Tuah’s viral podcast rant. And it resonates: she’s calling out the junior quant tendency to worship at the altar of the black box. The humor comes from how spot-on this critique is. It’s the classic Senior vs. Junior developers dynamic, transplanted into the world of trading algorithms. The juniors chase the latest shiny tech (here, deep neural networks, “non-linear methods”) with almost religious fervor, while the seniors (and here an influencer-style senior on a podcast) push back saying, “Cool your jets, kid, did you even check if that fancy model makes sense? Or are you just throwing math spaghetti at the wall?”

The meme’s two-panel image brilliantly juxtaposes the styles: on the left, we have Hawk Tuah in a cozy podcast studio, microphone at the ready, likely delivering this trending AI rant with a mix of passion and exasperation. On the right, we see the kind of academic vs. practitioner contrast that fuels her rant: a dense diagram of a neural network architecture with multi-modal inputs and a loss function full of Greek letters. It’s basically a slide from a research presentation. This split-screen tells a story. Hawk (the practitioner voice) is speaking in plain terms about overusing “advanced ML models,” and the slide next to her visually exemplifies those advanced models – it’s literally illustrating the complexity she’s talking about (multiple layers, lots of moving parts, plus a special feature_regularization_diagram to mitigate risk_of_overfitting). The visual gag is subtle: it’s almost like she’s pointing at that crazy diagram saying, “Look at what these juniors are doing – this is their idea of a solution!” For anyone who’s been in a quant research lab or a data science team, it’s quant_research_humor that hits close to home. We’ve seen that one team member who comes fresh from a machine learning course and proposes a monster neural network for even the smallest prediction problem, complete with colorful PowerPoint diagrams and equations – exactly like the right side of the meme.

Why is this funny and relatable? Because it’s true. Juniors often equate “more complex” with “more powerful.” If a linear regression didn’t find a pattern, they jump to a non-linear model with many layers and parameters, thinking surely the complexity will uncover hidden alpha. It’s like a reflex: problem? throw a neural net at it! – the pattern being satirized here is that many novices skip the basics (like exploring the data, trying simpler models, considering domain insights) and go straight to tuning a black box. In reality, black_box_models have their place but are not a panacea, especially in finance. The meme text even explicitly calls out “limitations of these models to deal with the high risk of overfitting.” Every senior quant can recount a horror story of an overfitted model. Picture a hedge fund junior excitedly proclaiming, “Our deep model had 98% accuracy on historical data!” The seasoned quant asks, “Alright, how about on out-of-sample or live data?” – and then comes the awkward silence or the painful admission that it tanked. It’s practically a trope in quant circles: brilliant backtest, dismal live performance.

Junior: “Look, I built this awesome 12-layer network. It finds amazing patterns in the last 5 years of stock data!”

Senior: “It will – probably the pattern of last quarter’ssignalnoise. How’s it doing on this quarter?”

That little dialogue encapsulates the AI_hype_vs_reality theme. The junior is filled with bravado (backtest bravado, we might say), while the senior delivers the reality check – echoing Hawk Tuah’s rant almost word for word. In quant terms, the ultimate judge is P&L (Profit and Loss). If your model makes money in live trading, great. If it doesn’t, all the fancy diagrams in the world mean squat. This is the P&L reality check that the meme mentions (in the alt-text: “often crashes into P&L reality”). Seasoned engineers have learned to be skeptical of anything that looks too good to be true on historical data, because they know how easily one can overfit models to chase past trends that won’t repeat. They likely have scars from real incidents: e.g., a black box trading strategy that worked amazingly until it encountered a slightly different market regime and then suddenly triggered a big loss. (As a cynical veteran might quip, “Nothing teaches caution like a model that loses a few million bucks the first week it goes live.”)

There’s also an undercurrent of academic_vs_practitioner tension. In academia, new MachineLearning papers often tout state-of-the-art results with complex architectures and just barely avoid overfitting by adding layers of regularization and careful validation. Junior researchers, especially those fresh from grad school or Kaggle competitions, tend to emulate that – they chase complexity because that’s what wins benchmarks or sounds impressive when publishing. In practice (especially in a profit-driven field like quant), the practitioner cares about robustness and interpretability. Simpler models might not be sexy, but if they are easier to interpret and trust, they can be preferable. A senior quant might say, “I’d rather have a 5-variable linear model I understand and can tweak, than a 5,000-parameter black box that I pray stays stable.” The meme plays on this mindset clash. Hawk Tuah’s rant is basically a practitioner’s plea: stop the AI hype train for a second and remember basic statistical rigor. It’s a call to not let the “black box worship” override common sense. And the fact it went viral implies a lot of people in the industry were nodding along vigorously – this podcast_rant struck a chord because many have been frustrated by that exact scenario.

It’s also a bit meta-funny: we have an influencer-like figure (podcasting has that vibe of modern “edutainment”) delivering what is essentially a grizzled engineering truth. It’s humorous that it needed to be said so plainly. The left image has her expression kind of like, “Guys… seriously?” – you can imagine the slightly exasperated tone: “These junior researchers keep picking the fanciest non-linear model without thinking about overfitting!” And the right image is essentially her evidence exhibit A: a convoluted network architecture (with a “feature network regularization” label, no less – translation: they know their model is so complicated it needs extra help not to shoot itself in the foot). The seasoned engineers viewing this meme chuckle because they’ve lived this: maybe not the exact neural network shown, but the endless cycle of overly complex solutions being hyped by newcomers. It’s AI humor with an edge of truth. Whether it’s a junior dev insisting on a bleeding-edge microservice architecture for a simple app, or a junior quant insisting on deep learning for a simple regression problem, the pattern is recognizable.

In summary, at the senior perspective this meme is highlighting Black Box Overkill in quant research. The combination of the tweet’s text and the images satirizes how juniors often default to maximal complexity (non-linear “magic” models) and have almost a blind faith in them (black_box_models as mysterious oracles). Meanwhile, experienced folks are reminding everyone that with great power comes great responsibility – or in this case, with great model complexity comes great risk of overfitting. The result is a gentle “I told you so” wrapped in humor: it’s funny because it’s true. All those colored nodes and fancy equations won’t save you when your overfit model meets fresh market data – an expensive lesson every overenthusiastic quant learns sooner or later. This meme’s popularity (viral tweet and all) shows that in the battle of hype vs. reality, the crowd secretly enjoys seeing reality poke a hole in hype. After all, there’s some schadenfreude in watching a black box idol get a bit of comeuppance from good old statistical common sense.

Level 4: Occam’s Chainsaw

At the deepest technical level, this meme highlights the classic trade-off between model complexity and generalization in machine learning theory. Junior quant researchers gravitating towards non-linear methods—like deep Neural Networks with lots of layers—are essentially wielding a chainsaw where Occam would suggest a simple razor. A linear model (think of a straightforward equation: prediction = w1*x1 + w2*x2 + … + b) has limited flexibility, so it can’t easily contort itself to every noise wiggle in the data. In contrast, a highly non-linear black-box model (picture the dense neural network diagram on the right side of the meme) has an enormous capacity to fit complex patterns. From a theoretical standpoint, such models have a high VC dimension and can approximate almost any function given enough parameters (the Universal Approximation Theorem). This power is a double-edged sword: it can learn the true underlying signal or happily memorize pure noise. Overfitting occurs when the model effectively memorizes the training data (including random fluctuations) instead of learning general rules – it’s as if the model becomes an overzealous student who memorized the answer key rather than understanding the lesson. The tweet mentions “high risk of overfitting” because in statistical learning theory, more complex models generally increase variance: they fit the training data extremely well but then generalize poorly to new, unseen data. Mathematically, if the model’s complexity grows too high relative to the amount of data (say the number of parameters >> number of independent data points), the interpolation error can approach zero on training data while the true predictive error balloons on test data.

In the right panel’s feature regularization diagram, we see an academic approach to taming this complexity beast. The diagram shows multiple neural nets (likely processing different modalities of data, labeled “modality 1” and “modality 2” with colored shapes), and then some combination layer $f(\cdot; W)$ and $g(\cdot; Z)$ feeding into a classification model. The equation at the bottom includes regularization terms: for example, a term $\alpha \sum (U_j - \sum_{S_j}U_j)^2$ and a $\beta | \ldots |^2$ term (it’s a bit blurry in the meme, but those form looks like penalty terms). This is essentially Tikhonov regularization (like an $L^2$ weight decay) or a specialized penalty to encourage the model not to overfit to one modality. In plain English, regularization adds a penalty for complexity: it’s a way to mathematically discourage the model from using overly convoluted parameter combinations unless they truly improve predictive performance. By adding those extra $\alpha$ and $\beta$ weighted terms to the loss function, the training process is forced to keep the model’s parameters in check (preventing any one sub-network from going berserk memorizing noise). We could express a simplified version of such a loss function as:

\text{Minimize}_{U} \Big[ \sum_{i} \ell\big(y_i, \hat{y}_i(U)\big) \;+\; \alpha \sum_{j}(U_j - \textstyle\sum_{S_j} U_j)^2 \;+\; \beta \|U\|^2 \Big]\,,

where $\ell(y_i, \hat{y}i)$ is the usual prediction error (like cross-entropy or MSE) for example $i$, and the extra terms are regularization: one could be encouraging different “feature networks” $U_j$ not to diverge too much from some shared structure (perhaps $\sum{S_j} U_j$ is an aggregation of related features), and the $\beta |U|^2$ term is a standard weight decay. The exact form aside, the presence of these terms confirms: the model is so complex that it needs heavy regularization to not overfit. This is a well-known paradox in advanced ML research – you design a super-expressive model, then immediately have to constrain it so it doesn’t learn nonsense. There’s a nod to the No Free Lunch theorem here: no single model is best for all problems, and adding complexity doesn’t guarantee better real-world results, it just shifts where you must be careful (here, careful via regularization and rigorous validation).

Historically, many quant finance veterans recall waves of enthusiasm for complex models. Non-linear methods like neural nets, kernel SVMs, or decision tree ensembles periodically trend as silver bullets. But seasoned quants know that financial data is notoriously noisy, non-stationary, and often low signal-to-noise. A method with too many degrees of freedom will overfit to past market idiosyncrasies (random coincidences, one-time events) that won’t repeat in the future. In academic literature, this is tied to the bias-variance tradeoff: simpler models (high bias, low variance) vs complex models (low bias, high variance). The juniors in this meme skew toward the low-bias/high-variance end without appreciating that high variance (model instability) is especially dangerous in finance – it leads to strategies that look amazing on paper and then mysteriously break when markets regime-shift or simply by random chance. The mention of “non-linear methods… despite the limitations of these models to deal with… overfitting” is essentially an admonition: deep nets and other complex algorithms can, in theory, fit anything (they’re universal function approximators), but in practice the limitation is our finite data and our noisy reality. You can’t cheat the fundamentals: overfitting models have weak generalization and can lead to catastrophic failures (like trades that blow up portfolios) when they meet the real world. In short, the deep technical joke is that while juniors treat machine learning like black magic, the math gods (in the form of statistical learning theory) demand their sacrifice – usually in the form of humility when the overfit model collapses. Occam’s Razor (favor simpler explanations/models) might be an age-old principle, but watching a junior charge in with Occam’s Chainsaw – a massively complex model – is both terrifying and darkly comical to those who know the theory. After all, if Occam’s Razor shaves with elegance, Occam’s Chainsaw slices indiscriminately – sure, it can carve intricate solutions, but it might also cut your trading account in half.

Description

A two-panel meme. The left panel shows Hawk Tuah, a woman with blonde hair, looking serious while speaking into a podcast microphone. The right panel displays several complex machine learning diagrams, including neural network architectures and scatter plots illustrating data classification. Above the panels, a tweet from "Stat Arb" (@quant_arb) reads: "Hawk Tuah recently went viral for her rant on the overuse of advanced machine learning models by junior quant researchers. 'Junior researchers prefer non-linear methods and complex black boxes despite the limitations of these models to deal with the high risk of overfitting'". The meme humorously juxtaposes a recent viral internet figure with a highly specific and technical critique of machine learning practices in quantitative finance. The joke lies in the absurdity of this crossover, while the underlying technical point about juniors preferring unnecessarily complex models and risking overfitting is a real and relatable issue for experienced data scientists and ML engineers

Comments

10Comment deleted

Juniors love neural networks for the same reason they love crypto: they don't fully understand how it works, but it looks great on a resume

If your Sharpe ratio evaporates the moment you disable dropout, you didn’t discover alpha - you overfitted a GPU-powered hallucination

Nothing says 'I understand finance' quite like throwing a 50-layer transformer at a problem that a simple linear regression solved in 1985 - but hey, at least the overfitting looks impressive in the quarterly deck to the partners who still think Python is a snake

Ah yes, the classic junior quant move: throw a 47-layer neural network at a dataset with 200 samples because linear regression is 'too simple' for your PhD. Meanwhile, the senior researcher is over here with a regularized logistic regression that actually generalizes to production, muttering 'I've seen this movie before' while your validation loss does the hockey stick of doom. But hey, at least your model architecture diagram looks impressive in the slide deck - right before it memorizes the training set and faceplants on real market data

Juniors spit neural nets at sparse tick data; seniors stick to linear regs that actually ship alpha

Pro tip from the old quant desk: if your strategy loses to a lasso with walk-forward validation and realistic slippage, you didn’t find alpha - you calibrated a random seed

If your Sharpe improves with the number of hyperparameters, you’re not modeling markets - you’re modeling your backtest harness

What does she think about the AGI revolution that is promised to us every other week? Comment deleted

hawk tuah spit on that thang Comment deleted

The what? Is it real? Comment deleted