Vibecoding Financial Products: A Networking Strategy With Legal Consequences

Why is this FinTech meme funny?

Level 1: The Lemonade Stand With Real Money

Imagine a kid who builds a lemonade stand by following instructions a robot shouted at him — and instead of selling lemonade, the stand somehow handles everybody's allowance, moves money between neighborhoods, and accidentally sends some of it to a man every grown-up has been told not to do business with. The kid says, cheerfully, "I've met so many interesting adults today!" — and the adults are lawyers, police officers, and a judge. The joke is that pride in "meeting new people" is hiding the fact that every one of those people showed up because he's in enormous trouble. It's funny because he's describing a disaster with the tone of someone describing a fun networking event.

Level 2: When Bugs Have Subpoenas

A quick decoder ring for the terms in play. Vibecoding means letting an AI write your code based on natural-language requests, accepting it if it seems to work, and iterating by feel rather than by reading and understanding every line. It's genuinely useful for prototypes — and genuinely terrifying in regulated industries, which are fields (finance, healthcare, aviation) where the law dictates how software must behave, log, and protect data.

Fintech — financial technology — covers payment apps, trading platforms, lending tools, and crypto exchanges (the @sherlock_hodles handle, a pun on "HODL," hints the author lives in crypto-adjacent territory). Building these requires licenses, identity verification of users, and reporting suspicious transactions. Skip those steps and the failure mode isn't a bad code review; it's the sequence the tweet lists: lawyers (you're being sued), police (you're being investigated), a judge (you're being prosecuted). Maduro is Venezuela's heavily sanctioned president — touching sanctioned money flows, even accidentally via code you didn't really read, escalates a hobby project into an international incident.

Early in your career, you learn that "it compiles" doesn't mean "it works." Fintech adds a third tier: "it works" doesn't mean "it's legal." That's why banks move slowly and why their codebases are full of compliance checks that look like bureaucratic noise until you understand what each one is keeping you out of.

Level 3: Move Fast and Break Statutes

The tweet — posted by rwlk (@sherlock_hodles) in classic X dark mode, complete with blue checkmark — lands because it compresses an entire risk-management seminar into two sentences:

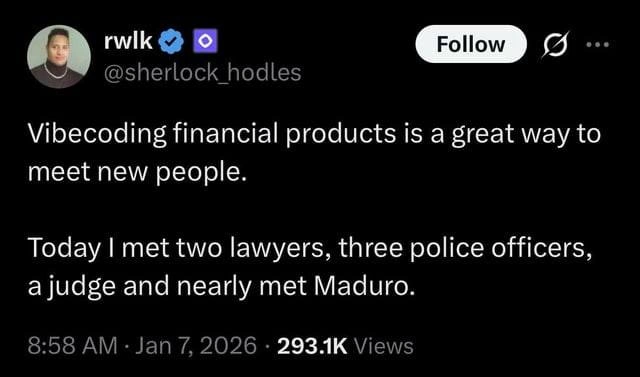

Vibecoding financial products is a great way to meet new people.

Today I met two lawyers, three police officers, a judge and nearly met Maduro.

Vibecoding is the 2025-era practice of building software by prompting an LLM, skimming the output, and shipping whatever vibes correctly. For a weekend side project, the worst-case outcome is a broken CSS layout. The joke's engine is domain mismatch: the author applied that workflow to financial products, the single most regulated category of software a civilian can write. Fintech code doesn't just have bugs; it has KYC/AML obligations, money-transmitter licensing, securities law, PCI-DSS, and audit trails that regulators actually read. A null-pointer exception elsewhere is a Sentry alert; in payments, a rounding error in someone else's favor is conversion, and an unlicensed exchange flow is a felony in several jurisdictions simultaneously.

The escalation ladder in the punchline is doing precise work. Two lawyers — civil exposure, probably a cease-and-desist or a contract dispute. Three police officers — now it's criminal. A judge — charges were actually filed; this is past the "strongly worded letter" phase. And then "nearly met Maduro" — the implication being the author's vibecoded product brushed against sanctioned entities or Venezuelan money flows, the kind of OFAC violation where the U.S. Treasury stops caring whether your code was AI-generated. The progression mirrors how compliance failures actually unfold: nobody notices for months, then everyone notices at once.

What experienced engineers recognize here is the deeper industry pattern: AI coding assistants flatten the perceived difficulty of domains without flattening their actual risk. The LLM will happily generate a custody wallet, an order-matching engine, or a cross-border remittance flow with the same cheerful confidence it generates a to-do app. The hard part of fintech was never the code — it's that the code encodes legal obligations the prompt author doesn't know exist. Code review by a senior engineer catches logic bugs; nothing in the vibecoding loop catches "this entire feature is illegal in New York." The 293.1K views suggest a lot of people felt that one in their compliance department.

Description

A screenshot of a tweet on X (dark mode) by user 'rwlk' (@sherlock_hodles), who has a blue verification badge and an avatar of a man in a white shirt with a chain necklace. The tweet reads: 'Vibecoding financial products is a great way to meet new people. Today I met two lawyers, three police officers, a judge and nearly met Maduro.' Posted at 8:58 AM on Jan 7, 2026, with 293.1K views; a 'Follow' button appears at top right. The joke skewers the trend of 'vibecoding' - building software by letting AI generate code without careful review - applied to the heavily regulated fintech domain, where bugs do not just crash apps but trigger lawsuits, criminal investigations, and regulatory action (the Maduro reference implying ending up in serious international trouble)

Comments

1Comment deleted

In fintech, 'ship it and see what breaks' is a fine strategy - it's just that what breaks is usually a federal statute