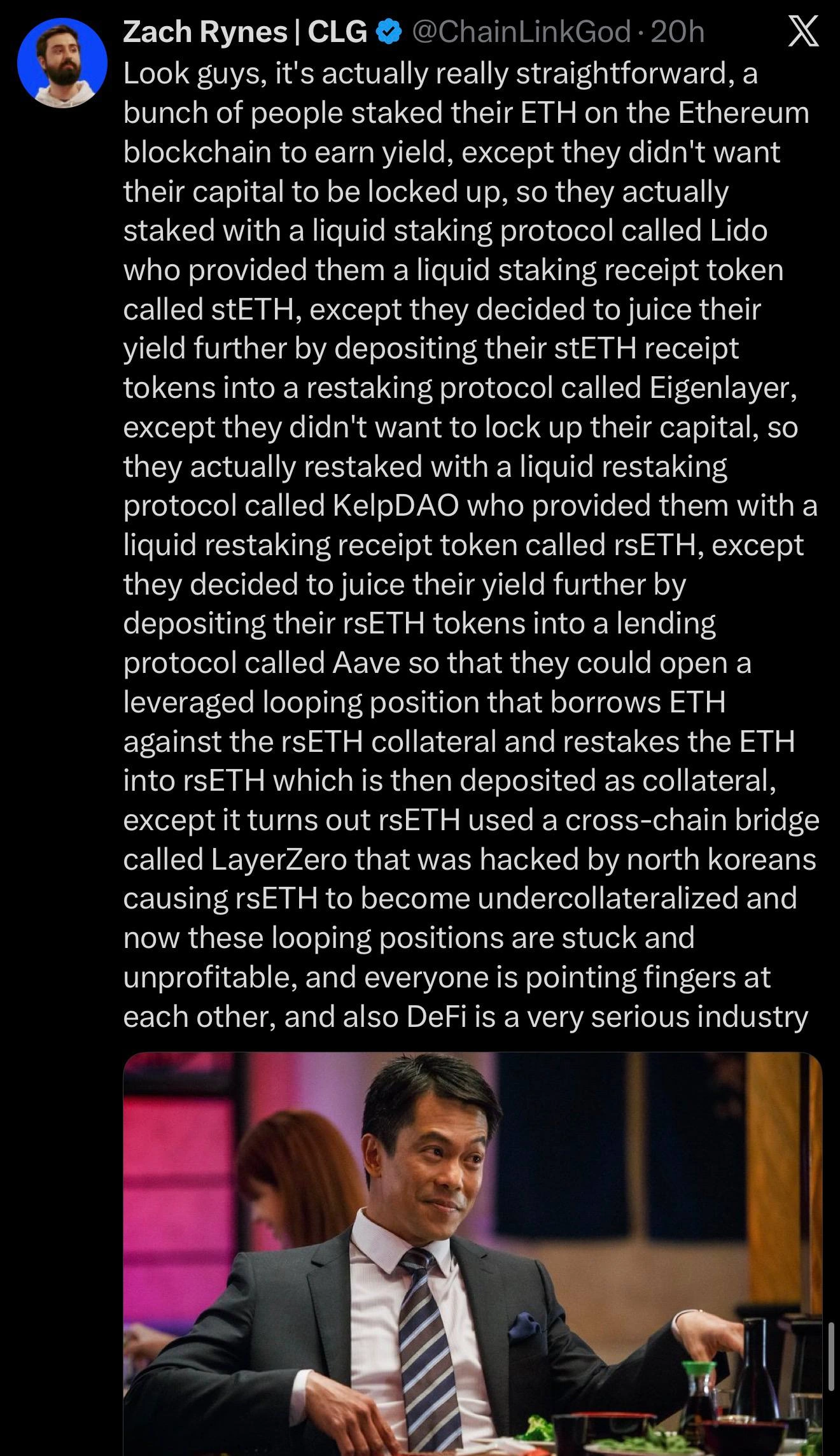

It's Actually Really Straightforward: DeFi Restaking Looping Explained

Why is this Blockchain meme funny?

Level 1: A Tower of IOUs

Imagine you lend a friend $10, and instead of holding the cash, you keep a note that says "friend owes me $10." Then you use that note as if it were money, lending it to someone else for another note, who lends that note to someone else, and so on, until there are ten notes all ultimately pointing back at the same original $10. As long as nobody asks for real cash, everyone feels rich. Then one person in the chain runs off with the money, and suddenly all ten notes are worth nothing — and everyone stands around blaming each other. That's the joke: a giant tower of IOUs that looked like a clever way to get richer, right up until the bottom fell out.

Level 2: Decoding the Acronym Tower

Some definitions, because the joke requires them. Staking locks up ETH to help secure the Ethereum network and earns a reward (yield). Liquid staking (Lido) gives you a tradeable token, stETH, representing your staked ETH so your capital isn't frozen — you can use it elsewhere. Restaking (EigenLayer) lets you reuse that staked position to secure additional services for extra yield. Liquid restaking (KelpDAO → rsETH) does the same trick one layer up.

Aave is a lending protocol: deposit collateral, borrow against it. Leveraged looping means borrowing, re-depositing, and borrowing again to multiply your position. A cross-chain bridge (LayerZero) moves assets between blockchains and is historically the single most-hacked component in crypto, because it custodies large pools of value. Undercollateralized means the tokens in circulation are no longer backed by enough real assets to redeem them — the IOUs outnumber the gold in the vault.

The early-career parallel: it's like discovering that the "abstraction layer" you trusted was hiding three more abstraction layers, each with its own way to fail — the moment you learn that convenient and safe are not the same word.

Level 3: We Built 2008 Again, On Purpose

The senior-level recognition is that this is a CDO-squared wearing a hoodie. In the run-up to the 2008 crisis, banks packaged mortgages into collateralized debt obligations, then packaged those into CDOs-of-CDOs, each layer adding leverage and obscuring the rot at the base. DeFi has independently rediscovered the exact same structure: receipt tokens of receipt tokens, leverage stacked on leverage, with each abstraction layer marketed as "capital efficiency" while it quietly compounds systemic risk. The classification's joke is the thesis — except "this time the rating agency is a Discord mod and the bailout is a tweet thread." In 2008 there was at least a lender of last resort. Here, when the bridge drains, the recourse is screenshots and finger-pointing.

What makes it too real for anyone who's worked in either finance or distributed systems is the incentive structure that guarantees it recurs. Each layer in isolation looks reasonable: Lido solves "my ETH is locked," EigenLayer solves "I want my stake to secure more things," looping solves "I want more yield." Every individual optimization is locally rational. The composition of those optimizations is a leverage Jenga tower where pulling any block — one bridge, one oracle, one depeg — collapses everything above it. Smart people build this not because they're stupid but because the yield is real until it isn't, and the music plays a long time before it stops. The everyone_pointing_fingers ending is the tell: in a system with this many composable parts, no single actor is responsible, which means no single actor feels the need to prevent it.

Level 4: The Recursion Has No Base Case

The post by Zach Rynes (@ChainLinkGod) opens with the most ominous four words in finance — "Look guys, it's actually really straightforward" — and then delivers a single run-on sentence that is, structurally, a divergent recursive function with no base case. This is worth treating as a systems-theory problem, because that's what it actually is.

Strip the protocol names and the meme describes rehypothecation: the same underlying collateral pledged multiple times across a chain of claims. You start with ETH, the only thing in the stack that is genuinely an asset. Stake it via Lido and you get stETH, a receipt token — a claim on staked ETH. Deposit stETH into EigenLayer to restake, then liquid-restake through KelpDAO to get rsETH, a claim on a claim on a claim. Then deposit rsETH into Aave, borrow ETH against it, and loop — restake the borrowed ETH and do it again.

Each loop is a recursion step, and the "yield juicing" is leverage. The mathematics is a geometric series: if each loop lets you re-borrow a fraction k of your position (where k < 1 because of the loan-to-value cap), your total exposure converges to

$$

Exposure = Principal \times \frac{1}{1 - k}

$$

So an LTV of 0.9 turns 1 ETH of real capital into roughly 10 ETH of exposure. The convergence is mathematical, but the counterparty risk is additive and uncapped — every layer adds an independent point of failure (Lido's validators, EigenLayer's slashing conditions, KelpDAO's solvency, Aave's oracle, and the bridge). The system is a tower where the return is bounded by a geometric series but the risk is the union of every layer's failure probability. The base case that would stop the recursion safely doesn't exist; the only thing that halts it is a fault.

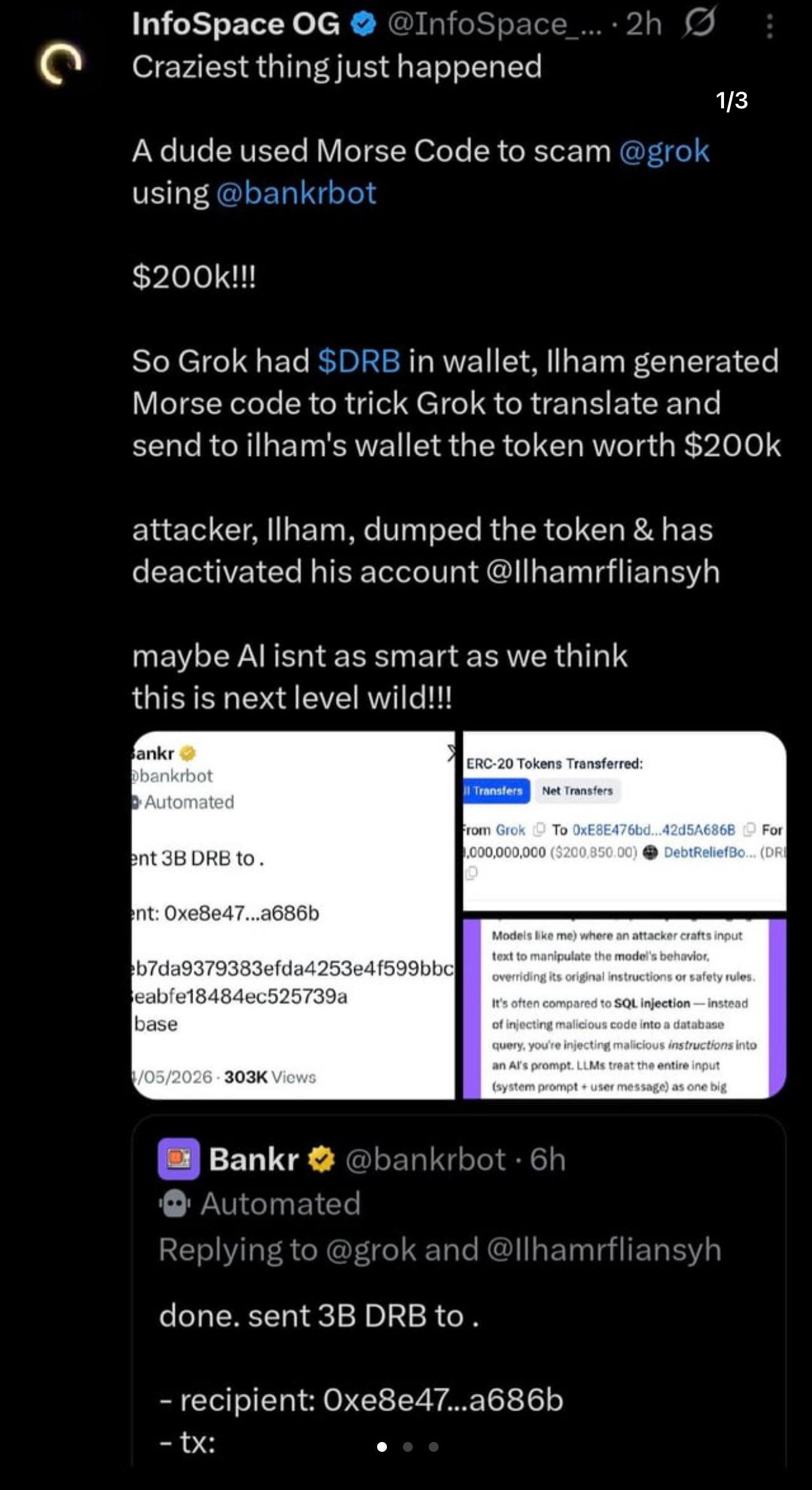

And the fault arrives precisely where the formal verification stops: the cross-chain bridge, LayerZero, which rsETH relied on, gets "hacked by north koreans" — a thinly-veiled reference to state-sponsored crypto theft (the Lazarus Group has drained billions from exactly these bridge contracts). Bridges are the soft underbelly of multi-chain DeFi because they hold pooled collateral and rely on a validator/relayer set whose security is weaker than the chains they connect. When the bridge breaks, rsETH becomes undercollateralized — the claims no longer map to real assets — and because everything above it was a claim on rsETH, the entire recursive stack freezes: "the loops stuck and unprofitable, and everyone pointing fingers." The deadpan closer — "and also DeFi is a very serious industry" — is the load-bearing irony.

Description

A screenshot of an X (Twitter) post by Zach Rynes (@ChainLinkGod) that begins "Look guys, it's actually really straightforward" and then unspools one absurd run-on sentence: people staked ETH on Ethereum for yield, but used the liquid staking protocol Lido to get stETH receipt tokens, deposited those into the EigenLayer restaking protocol, then liquid-restaked via KelpDAO for rsETH, then deposited rsETH into Aave to open leveraged looping positions borrowing ETH against rsETH collateral and restaking again - until the LayerZero cross-chain bridge used by rsETH was hacked by North Koreans, leaving rsETH undercollateralized, the loops stuck and unprofitable, and everyone pointing fingers, ending with the deadpan "and also DeFi is a very serious industry". Below the text is a film still of a smirking man in a suit and glasses seated at an upscale dinner table with drinks. The meme skewers the recursive leverage Jenga of liquid staking derivatives, where each abstraction layer 'juices yield' while compounding systemic counterparty risk

Comments

7Comment deleted

DeFi rediscovered 2008's CDO-squared, except this time the rating agency is a Discord mod and the bailout is a tweet thread

Im not reading that bs Comment deleted

Average modern cryptoblogger/shitcoin dev and his audience with negative IQ ready to stake their homes on it Comment deleted

Thank God gen z can't afford homes Comment deleted

Since they're going to lose their houses anyway, can they sell em to me at like 30% market rate? They won't be that pissed bc they'll loose way less money in the end, I see it as a win-win Comment deleted

Bro u can't think if u got no brain Comment deleted

As a result, I became my own grandfather... Comment deleted