Ransomware ROI: Hack the Insurer, Hit Only the Pre-Approved Payers

Why is this Security meme funny?

Level 1: Bully’s Lunch List

Imagine you’re at school, and there’s a bully who wants to steal lunch money. Now, this bully could randomly pick on kids and hope they have some money… but the bully does something sneakier. He manages to peek at the teacher’s list that shows which kids pay for lunch or bring money to school every day. Suddenly, the bully knows exactly which kids definitely have lunch money. Those kids become his top targets, because he’s sure they have something to steal.

In the story from the meme, the “bully” is a group of bad hackers (a ransomware gang). The “lunch money” is the ransom money companies might pay when their computers get locked by a virus. And the “teacher’s list” is the customer list of an insurance company. Some companies buy cyber insurance, which is like a promise that if hackers attack them, the insurance will pay the ransom or help them recover. The hackers found this out, and it’s as if they secretly looked at the insurance company’s files to see which companies had bought this protection. Those companies are like the kids definitely carrying lunch money. So the hackers said, “We choose to attack those ones,” because they knew those companies had a high chance of paying the ransom (since the insurance would cover it).

It’s a bit funny in a twisted way, right? The very thing meant to protect you (insurance, or a school program to ensure kids have lunch) ended up helping the bad guys pick their victims. It’s like if the bully heard that any kid who gets their lunch money stolen will be given new lunch money by the school – that bully would then only steal from those kids, knowing the school will refill their wallets, maybe even multiple times! The meme makes us grin because it shows how clever (and sneaky) the bad guys can be, turning a safety net into a target map. But it’s also a little scary – it reminds us that we have to be careful, because sometimes our solutions (like insurance) can create new problems if the “bullies” figure them out.

Level 2: Hacking the Insurer

Let’s break down what’s going on in simpler terms. Ransomware is a type of malicious software (malware) that locks or encrypts a victim’s files, effectively holding data hostage until a ransom (money, often in Bitcoin or another cryptocurrency) is paid. It’s one of the nastiest kinds of SecurityIncident an organization can face – imagine all your servers and workstations suddenly displaying a note: “Your files are locked. Pay us $1,000,000 to get the decryption key.” It’s digital extortion.

Now, many companies have started buying cyber insurance, which is like an insurance policy specifically for cyber attacks and data breaches. If a company with cyber insurance gets hit by ransomware, the insurance can cover the costs – for example, paying the ransom, hiring experts to recover data, notifying customers of a breach, etc. It’s similar to how having car insurance helps if you get in an accident. The idea is to transfer some of the financial risk to the insurer. This sounds smart, right? However, here comes the twist.

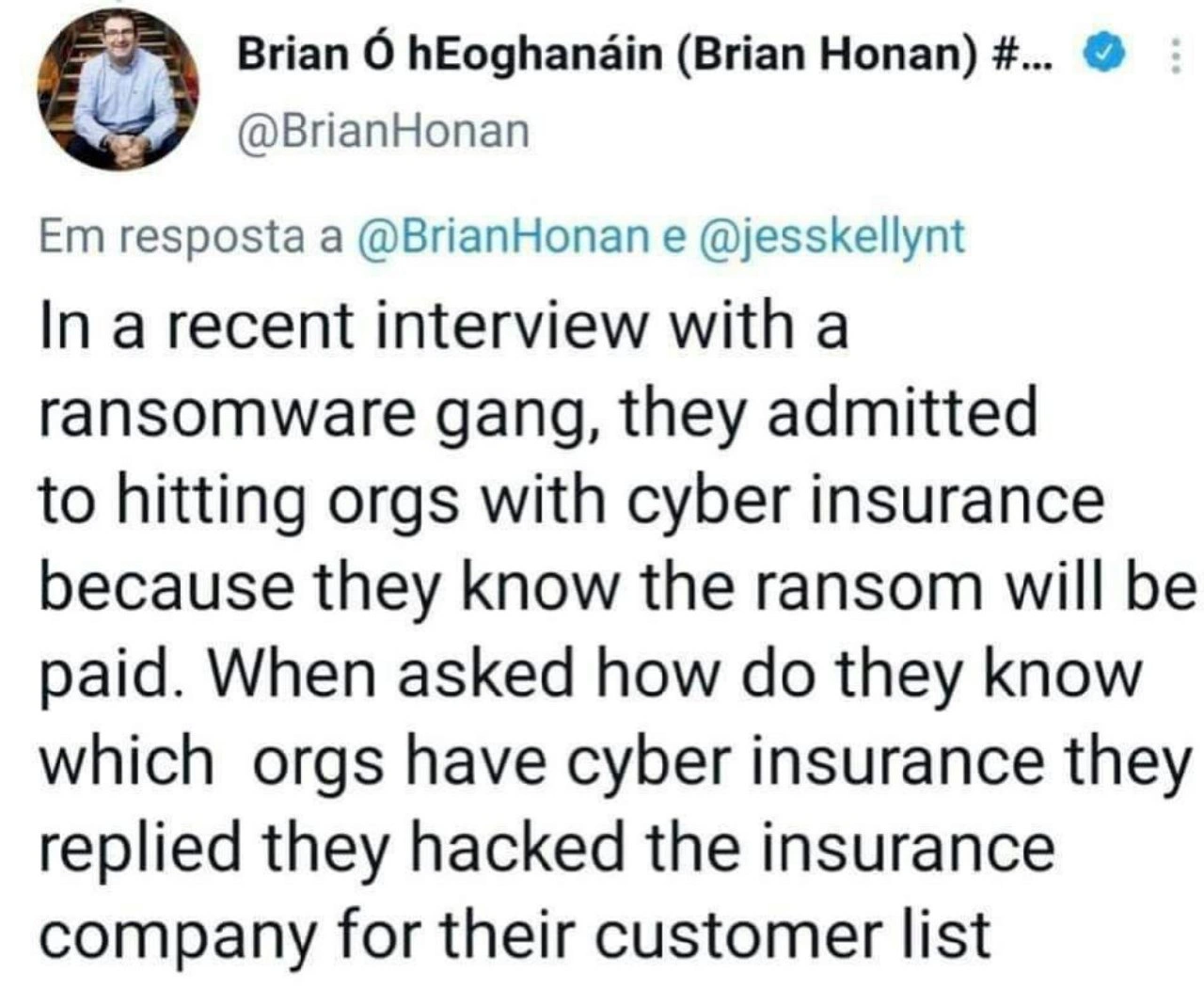

The tweet describes an interviewer talking to a ransomware gang (the group of hackers/criminals who carry out these attacks). The gang admitted that they deliberately target organizations that have cyber insurance because they know those companies are likely to pay the ransom. Why would they pay? Because their insurance policy literally will pay out for them. The attackers are basically saying, “We prefer victims who have a kind of safety net that guarantees we get our money.” It’s as if a kidnapper only kidnaps people whose family has a kidnap-ransom insurance – because they know the insurance will pay the ransom promptly. In practice, insurers often do end up paying ransoms (sometimes reluctantly) to resolve cases, which has signaled to criminals that insured victims are reliable payers. This is a huge security tradeoff: having insurance helps cover the cost of an attack, but it also might make you more attractive to attackers in the first place.

Now the obvious question: How do criminals know which organizations have cyber insurance? That detail is the punchline of this meme. The ransomware gang said they found out which companies are insured by hacking the insurance company itself to steal their client list. In other words, they breached the very company that sells those cyber insurance policies. This is a form of supply_chain_breach or third-party breach: instead of attacking a target directly, hackers go after a related entity that holds valuable information. Here, the insurer is a vendor that had a database of all its customers (other companies) and likely details about their policies. By hacking the insurer, the criminals got a treasure trove of data: a list of organizations and possibly notes on their coverage (maybe even how much ransom the insurer would cover). That’s like a menu of the best possible victims. This is a glaring example of vendor_risk – when you trust another company with your sensitive data, you’re exposed to their security weaknesses. If they get breached, your data (in this case the fact you have insurance) gets exposed.

So, the sequence is: an insurance_company_hack led to a DataBreach (leak of the customer list). Armed with that list, the ransomware gang could cherry-pick who to attack, knowing in advance that these targets likely have funds ready to pay. This is extremely efficient for the criminals: it’s targeted marketing in the underworld. Why send phishing emails to 10,000 random companies when you can send them to 100 companies you know have the means (and insurance policy) to pay ransom? This strategy of attack_target_selection shows how organized and calculated ransomware operations have become. They treat it like a business: maximizing profit and minimizing effort. It’s frankly a scary development in ransomware_economics – the financial side of cybercrime.

The humor or irony in the meme comes from how backwards this situation is. Cyber insurance was supposed to help mitigate risk and give organizations peace of mind. Instead, it inadvertently acted like a beacon for attackers: “We have money set aside for hackers.” The tweet highlights that the ransomware gang openly revealed this tactic, which is both shocking and darkly funny to those of us in security. It’s like a thief saying, “Of course I rob houses with alarm company signs out front – I stole the alarm company’s client list, so I know which houses have insurance to cover the theft!” It’s a head-shaking moment that shows the unintended consequences in cybersecurity – every defense or safety measure can introduce a new vulnerability or SecurityFlaw if we’re not careful.

Level 3: Premium Targets

For seasoned security engineers, this scenario provokes a facepalm and a grim smirk. It’s a perfect storm of SecurityTradeoffs coming home to roost. Consider the irony: companies bought cyber_insurance to mitigate ransomware risk, expecting an insurer to cover the ransom or recovery costs. But that very practice painted a huge bull’s-eye on their backs. The ransomware gang effectively said, “We target orgs with insurance because we know the ransom will be paid.” In other words, they go after premium targets – organizations pre-approved by an insurer to have the funds (and likely the willingness) to pay up. It’s criminal attack_target_selection at its most ruthlessly efficient: skip the hard sells and go straight to the customers who’ve signaled they have a budget for your “service.”

How did the gang know who’s insured? They didn’t consult a crystal ball or guess – they hacked the insurance company itself. Yes, the very firm writing cyber policies got compromised, coughing up a list of all its customers. That’s a classic supply_chain_breach: instead of attacking a hundred companies one by one, hit one hub that connects to those hundred. In this case, the insurance provider was the hub holding sensitive client data. This is a nightmare scenario for DataPrivacy and vendor trust – a vendor_risk fiasco where the guardian of risk information became the single point of failure. The attackers turned an insurance_company_hack into a shopping catalog of victims.

The humor here is bone-dry and bitter: it’s as if the burglars robbed the locksmith to steal a list of homes with the fanciest locks – because those homeowners are definitely worth robbing. Security veterans have long muttered that paying ransoms (especially via insurance) fuels the ransomware economy. Now we have a blunt confirmation straight from the wolf’s mouth. The ransomware gang basically admitted their business runs on the ransomware_economics of guaranteed payouts. They’ve managed to weaponize an insurance policy into an assurance of criminal revenue. It’s the ultimate “thank you for your business” moment – insurers quietly paying ransoms to resolve incidents have inadvertently told criminals, “These folks will pay, come on down!” You can almost hear the cynical laughter in IT departments: “Of course they hacked the insurer… that’s exactly what we would do (if we had no soul)!”

This also underscores a SecurityFlaw in how organizations and insurers handle ransomware. Insurers often require their clients to follow certain security practices (so-called “we’ll insure you if you have multi-factor auth, backups,” etc.), but clearly not all vulnerabilities can be closed – especially not at the insurer itself. When the insurer got breached, it betrayed its clients en masse. It’s a reminder that your security is only as strong as the weakest link in your ecosystem – and sometimes that link is a big, well-funded insurance firm that you assumed was ironclad. For senior folks, it’s a rueful chuckle: the industry tried to treat ransomware as a financial problem to be insured away, and the criminals responded by treating the insurance as their to-do list. It’s outrageously clever and absolutely devastating — the kind of thing that in an IR (Incident Response) post-mortem would make everyone in the room go silent for a moment. Then the cynical veteran in the corner would snark, “Well, what did you expect? They basically gift-wrapped the target list.”

Level 4: Moral Hazard Heist

At the most theoretical level, this twist of fate highlights a perverse form of economic game theory in cybersecurity. Ransomware gangs aren’t just script-kiddies poking random servers; they’re effectively running a data-driven business optimizing for ROI (Return on Investment). Here, the attackers exploited information asymmetry: by breaching the cyber insurer (the keeper of who’s insured), they eliminated uncertainty about which targets will pay. This is akin to adverse selection in insurance economics, but in reverse – the adversaries are doing the selecting. It’s a darkly brilliant strategy: why waste bandwidth phishing random companies when you can compile a list of pre-qualified leads guaranteed to have ransom money set aside? It’s the Nash equilibrium of ransomware economics – as long as insurers implicitly guarantee payment, attackers gravitate toward those insured, reinforcing a vicious cycle.

From a security economics standpoint, it’s a textbook example of moral hazard: organizations with cyber insurance might be less incentivized to harden defenses (since a payout is available), and attackers know it. The very safety net (insurance) creates a target market signal – a juicy guarantee that ransoms will be paid promptly by a deep-pocketed third party. In essence, the insurer’s customer database became a treasure map. This scenario exposes a systemic SecurityTradeoff: transferring risk via insurance can inadvertently concentrate risk elsewhere. Academically, it resonates with Ross Anderson’s theories on the economics of information security, where misaligned incentives often lead to worse security outcomes. When the “good guys” aggregate sensitive data about who is protected, the bad guys see an opportunity for a supply_chain_breach with maximum payout. The result is an almost inevitable equilibrium in the ransomware ecosystem – a calculus where criminals invest in one high-effort insurance_company_hack to reap the compounded reward of multiple guaranteed-paying victims. It’s a heist not of money directly, but of risk intelligence – the ultimate moral hazard exploit, turning the insurance model on its head for criminal gain.

Description

Screenshot of a tweet on a white background with Twitter’s standard blue accents. The avatar shows a blurred person in a blue shirt, user name “Brian Ó hEoghanáin (Brian Honan) #…” and handle “@BrianHonan.” A light-blue reply banner reads “Em resposta a @BrianHonan e @jesskellynt.” The tweet text says: “In a recent interview with a ransomware gang, they admitted to hitting orgs with cyber insurance because they know the ransom will be paid. When asked how do they know which orgs have cyber insurance they replied they hacked the insurance company for their customer list.” Visually it’s plain text, but technically it underscores the attacker’s business-driven targeting logic, the irony of supply-chain breaches, and the unintended incentives created by cyber-insurance markets

Comments

7Comment deleted

When your threat intel feed is literally the insurer’s customer CSV, the kill chain becomes more of a billing workflow

The ultimate catch-22: buying cyber insurance is like putting a 'I have money' sign on your back in a dark alley full of hackers. The insurance company's customer database becomes the ransomware gang's CRM system - talk about a perverse form of lead generation

The ransomware gang essentially performed a SELECT * FROM insured_targets WHERE likely_to_pay = true; - proving once again that the real vulnerability isn't in your firewall, it's in your business model. They've effectively turned cyber insurance from a risk mitigation strategy into a targeting beacon, creating a beautiful recursive security failure where the protection mechanism itself becomes the attack vector. It's like putting a 'Protected by ADT' sign on your lawn, except the burglars hacked ADT's customer database first

Ransomware gangs just perfected supply-chain attacks: Hack the insurer's CRM once, auto-target payers forever. Vendor risk audits intensify

Turns out “risk transfer” was the attackers’ data-enrichment pipeline: ETL from the insurer’s CRM to a guaranteed cashflow target list

Ransomware finally nailed product - market fit: ICP = “has cyber insurance,” data source = “insurer CRM,” pricing = “policy limit,” and their sales ops updates the pipeline faster than ours

I think the insurance company need an insurance 😅 Comment deleted