Startup nostalgia: zero rates, NFT millions, and the valuation crash

Why is this Startup meme funny?

Level 1: No More Free Candy

Imagine you and all your friends are at a magical candy store where, for a long time, candy was free. Every day you could walk in, grab as many gummies and chocolate bars as you wanted, and it wouldn’t even cost a penny. You all got used to this – everyone’s pockets were overflowing with candy, kids were trading bubble gum like it was treasure, and everyday felt like a party because the candy supply was endless. Some kids even started trading silly stickers (like those shiny Pokémon cards or cartoon stickers – kind of like digital pictures in a way) for tons of candy because why not? Candy was free and everyone was excited about collecting the coolest sticker or sweet. It was almost too good to be true, but it went on for a while, and all of you thought it would last forever. It was perfect, like a fun machine that never broke: take candy, have fun, trade things for candy, get more candy – easy!

Now imagine one day the store owner announces, “Sorry kids, candy isn’t free anymore. We have to charge money now.” Suddenly, everything changes. You reach for a lollipop and someone says, “That’ll be $2.” Your jaw drops. You look in your piggy bank and realize you can’t get sacks of candy like before. You maybe can buy one lollipop a week if you save up. Overnight, the candy party is over. Those shiny stickers that kids were trading for heaps of candy? Now that candy isn’t free, fewer kids want the stickers at all, because who’s going to trade real money for them? Their value plummets – something that a day ago you could swap for 10 candy bars, now no one will even give you a single candy cane for it.

In our story, some kid (or maybe the store owner, or just the situation) “ruined” the fun by ending the free candy era. One of the older kids might throw a tantrum, yelling: “We had it so good! We had free candy, unlimited treats, everyone was happy, everything was working perfectly – and now you messed it up!” They’re just super upset that their magical free-candy world disappeared.

That’s exactly what this meme is about, but instead of candy it’s talking about money and startups. The grown-ups had a period where money felt free (they could get lots of it to fund their projects), everything was going great and prices for things (even goofy things like digital pictures of apes) were sky-high. Then the world changed, the free money went away (kind of like the candy no longer being free), and everything came crashing down in value. The people in tech are jokingly acting like kids who lost their free candy, shaking their fist and saying “we had it all and it was ruined!”

It’s funny in a kinda sad way: it shows how people can get so used to good times that when things go back to normal, they react dramatically. Just like you’d laugh a bit seeing a kid dramatically lamenting the end of free candy, the meme makes us laugh seeing tech folks lamenting the end of the “free money” days. The big feelings are the same – “those were the best times ever and now they’re gone!” – and whether it’s candy or money, we can all understand that feeling.

Level 2: Bubbles and Busts

During the past few years, the tech startup world went through a boom-and-bust cycle that this meme is joking about. In simple terms, there was a “perfect storm” for startups that made everyone feel like geniuses — until it suddenly ended. Let’s break down the parts of the tweet to understand what each means in real life:

- Zero rates: This refers to near 0% interest rates. Central banks (like the Federal Reserve in the US) set very low interest rates from the 2010s through 2021. When interest rates are zero, borrowing money is super cheap. Investors can get money easily and aren’t paying much interest on it, so they’re willing to pour money into investments that are riskier (like new tech startups) because even safe investments (like bonds) aren’t paying anything. Essentially, money was “free” in a sense, encouraging people to invest in all kinds of ventures.

- Unlimited startup funding: Because money was so cheap and plentiful, venture capital firms (the investors who fund startups) had tons of cash to invest. Startup funding exploded — companies that were just an idea or had a small product could raise millions of dollars. It felt “unlimited” because every time a startup needed more money, there was some VC ready to cut a check. This is very different from normal times when only a few startups get a lot of funding; here, almost everyone with a half-decent idea could get funded. Startups were using this money to grow fast (often without worrying about making profit immediately).

- Soaring valuations: A company’s valuation is how much it’s worth on paper (often determined by the price investors pay for a share of it in a funding round). “Soaring valuations” means these numbers were sky-high and kept rising. For example, a tiny startup might be valued at $50 million one month, and then after some growth or just a new round of hype, suddenly investors value it at $500 million. Many startups became “unicorns” (valued over $1 billion) quickly. These valuations were soaring because investors were optimistic (some might say overoptimistic) about future success, fueled by all that available money and a fear of missing out on the next big thing.

- JPEGs that sold for millions: This sounds bizarre, and it kind of is. It refers to the NFT craze. NFTs (Non-Fungible Tokens) are a type of digital asset on the blockchain. Non-fungible just means each one is unique. In practice, most NFTs were basically digital collectibles, often linked to a digital image (like a JPEG picture file). For instance, there were collections of digital art like the “Bored Ape” cartoons or pixelated characters called CryptoPunks. Owning an NFT of one of these means your name is on a blockchain saying you own that specific digital picture. During the boom, people started paying millions of dollars for these NFT images. Yes, literally – an image that you could copy on your computer, but because it had a token saying “this is the original”, folks treated it like fine art. So when the meme says “JPEGs that sold for millions,” it’s highlighting how even something as seemingly silly as a digital picture of an ape or a pixel art character was fetching huge sums of money. This was a real trend in 2021: it was the ultimate symbol of how wild and hype-driven the market had become.

- Everything we needed and it all ran like clockwork: “Ran like clockwork” means everything was working perfectly, smoothly, and predictably. In context, it’s saying all these conditions – free money (zero rates), tons of funding, high valuations, NFT mania – created a kind of well-oiled machine for the tech industry. Startups would get funded easily, use the money to grow, which made their valuations go up, which then attracted even more funding, and even side-crazy things like NFTs kept going up in price too. It paints a picture that this system was working and everyone was winning. It’s a bit sarcastic, because obviously this was too good to go on forever, but at the time it really did feel like a golden period where everything was falling into place for tech companies.

So the tweet is listing these points to reminisce about that crazy time. Why the past tense “We had…”? Because it’s over now. The meme is lamenting (in a joking way) that this great setup is gone.

What changed? In 2022, those zero interest rates disappeared. Inflation picked up in the wider economy (prices of everyday goods were rising), so central banks raised interest rates to cool things down. When interest rates went up, money wasn’t so free anymore. Borrowing became expensive, investors got more cautious (since safe assets like bonds started giving decent returns again), and suddenly that flood of VC funding dried up. Startups that could once easily get another round of millions found that investors were now asking tough questions like “Are you profitable? What’s your revenue?”. Many startups that had been burning cash to chase growth had to slam on the brakes. In real terms, this meant layoffs (companies had to cut costs because they couldn’t keep spending money they no longer had), down rounds (some startups had to raise money at a lower valuation than before, which is like an embarrassing reality-check on their true worth), or even shutting down. The whole vibe shifted from “grow at all costs” to “survive at all costs”.

And those NFTs? They largely crashed in value. The same “JPEGs” that sold for millions found few buyers in 2022 and 2023. The NFT market volume fell drastically. It turned out a lot of people bought NFTs hoping to resell them for more money (speculation). When the bubble popped, they realized not many genuinely wanted to pay high prices for these digital collectibles once the hype was gone. So NFT owners saw their investments plummet. For instance, an NFT that someone bought for $1 million might struggle to sell for $100k or even $10k after the crash. The bubble had burst.

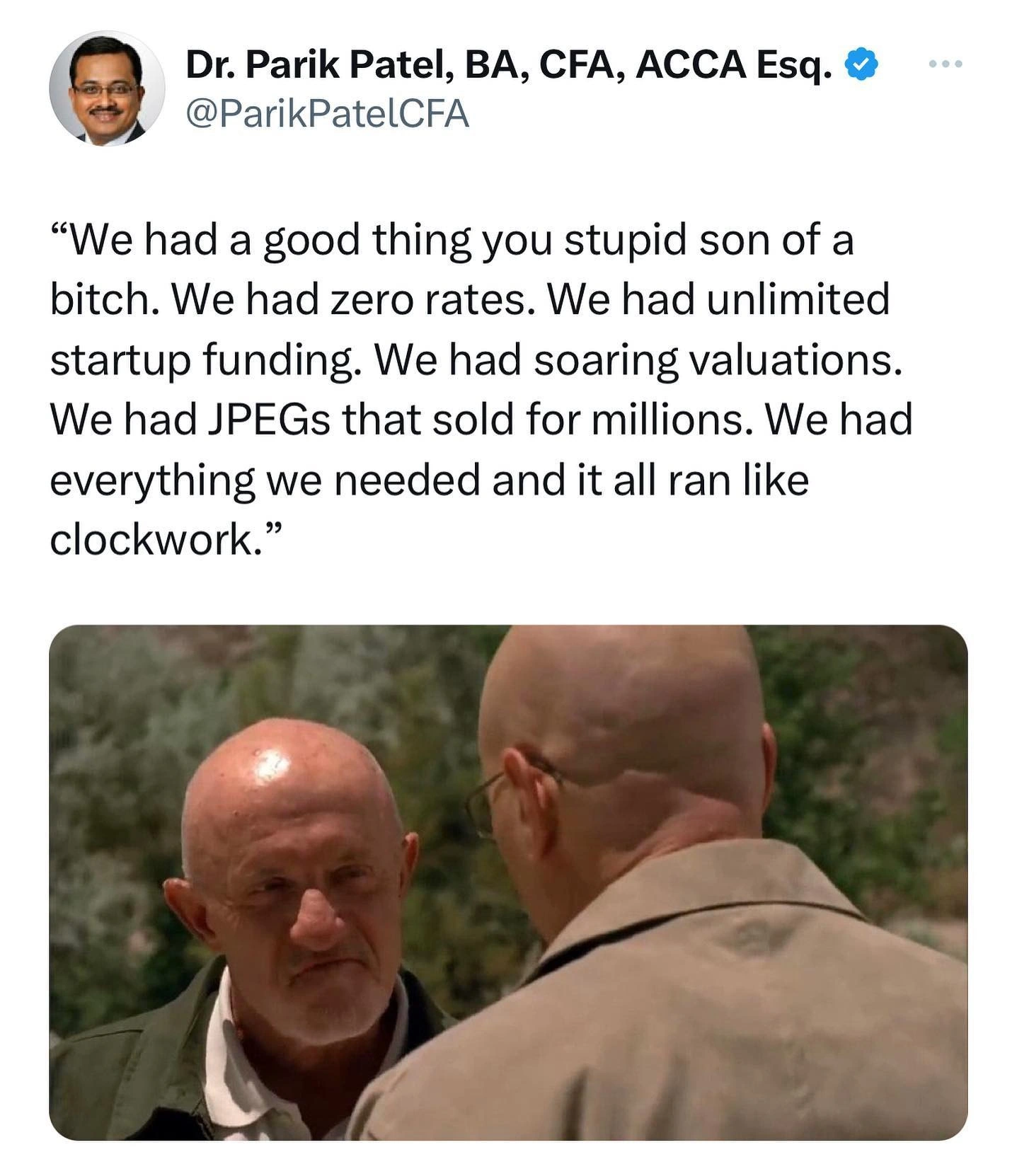

The meme uses a scene from Breaking Bad (a famous TV show) to dramatize this situation. The image with the two bald men in the desert is from that show – it’s an intense confrontation. By quoting that scene (“We had a good thing you stupid son of a b****…”), the meme is pretending like someone from the tech world is yelling at whoever “ruined” the good times. It’s a bit of dark humor. Essentially, the person in the meme is shouting: “We had it all! Free money, tons of funding, huge valuations, even silly NFTs making millions – it was perfect! And now it’s gone.” In Breaking Bad, it was one character’s fault that the good setup fell apart. In the tech world, it’s not one person but a change in the economic environment (interest rates going up, investors pulling back) that “ruined” it. Still, the meme jokingly acts like it was a betrayal or someone’s dumb decision that ended the party.

For a junior developer or someone new to the industry, this meme is basically a history lesson of 2019-2021’s wild tech ride packaged as a joke. The tone is sarcastic nostalgia. People are mockingly “nostalgic” for those boom days. It’s funny because everyone knew it couldn’t last, but the way it’s phrased feels like an angry complaint that it ended – which is kind of true emotionally for some folks! If you joined a startup during the boom, you might have thought “this is normal” – free lunches, big hiring plans, valuations doubling – and then suddenly you’re in a bust where budgets are slashed and you’re lucky if you keep your job. That reversal is shocking.

So, the meme resonates by putting into words what a lot of tech people experienced: whiplash. It educates through humor: we hear about the tech hype cycle (massive hype followed by a crash) all the time, but here it’s personified as this angry rant. Reading it, you learn that:

- The tech industry had a huge bubble (the boom times with low interest, lots of funding, NFT craziness).

- That bubble popped (interest rates rose, money got tight, everything came crashing down).

- People in the industry felt this change very strongly – and now they’re making jokes to cope with it.

In short, Level 2 take-away: the meme is saying “Remember how crazy things were when money was practically free? We could fund anything, valuations were insane, we even sold silly digital pictures for millions. It all worked smoothly… until reality hit and the bubble burst.” It’s a way for those who went through it to explain the story with a laugh (and maybe a groan). Even if you’re new and didn’t experience it directly, you can understand it as a recent chapter of startup history – one that people will be talking about for years as a cautionary tale of hype and crash.

Level 3: Valuation Whiplash

“We had a good thing you stupid son of a b****. We had zero rates. We had unlimited startup funding. We had soaring valuations. We had JPEGs that sold for millions. We had everything we needed and it all ran like clockwork.”

This meme is industry satire at its finest, channeling a famous Breaking Bad scene to capture the whiplash tech has felt in going from boom to bust. The tweet text above almost directly quotes Mike Ehrmantraut’s furious monologue to Walter White, but repurposes it for the startup world. In the show, Mike angrily reminds Walt that “We had a good thing… we had Fring, we had a lab… it all ran like clockwork” until Walt’s ego ruined it. In the meme, our “good thing” wasn’t a clandestine meth empire, but rather the absurdly perfect conditions of the late 2010s and 2020-2021 tech boom. Zero rates (near-zero interest rates) were the equivalent of Gustavo Fring — a powerful force keeping everything smoothly running. With cheap money as the silent partner, unlimited startup funding flowed and every crazy tech idea got its day in the sun. Like Walt messing up the operation, something (or someone) “stupid” messed up these perfect conditions — likely a tongue-in-cheek swipe at the Federal Reserve raising rates, or at least at the collective hubris that assumed the party would never end.

Senior engineers and founders reading this meme are nodding (or smirking) because they recognize every element in that rant as a reality they just lived through. It tickles that shared memory (half exhilarating, half traumatic) of an era when tech was awash in cash and hype. Let’s break down the litany of “We had…” goodies being mourned:

- Zero rates – For years, interest rates were effectively 0%. This zero-interest-rate policy fueled easy credit and made venture capital extremely eager to invest. From a startup perspective, it was like gravity had been turned off in finance: money was weightless and everywhere.

- Unlimited startup funding – Because money was so cheap, VCs were writing huge checks to any promising venture. Seed rounds turned into eight-figure Series A’s, and venture funding glut became the norm. Startups with minimal traction could raise multiple rounds just on potential. Companies didn’t worry about running out of cash (runway); if you needed more, you’d just raise another round at an even higher valuation.

- Soaring valuations – Every funding round seemed to double or triple a company’s paper value. A unicorn (startup worth >$1B) was no longer rare; by 2021, it felt like new unicorns were minted weekly. This is the “up-and-to-the-right” mentality: all charts (user growth, revenue projections, valuation) only pointed skyward. Investors were valuing companies not on present earnings (often there were none) but on rosy future narratives. This is the era when a startup for renting expensive digital cats or a company delivering burritos by drone could be worth billions. It sounds insane – and it kind of was – but in that climate it seemed normal because everyone was playing along.

- JPEGs that sold for millions – Perhaps the most absurd emblem of the era: the NFT bubble. People were buying NFTs (which are essentially digital certificates of ownership for images or other digital items on the blockchain) for eye-popping prices. Think of CryptoPunks (pixelated 8-bit style heads) or Bored Ape Yacht Club cartoons selling for hundreds of thousands or even millions of dollars each. These are literally JPEG image files (often profile pictures), except now there was a token proving you “owned” that image. In late 2021, stories of someone flipping a meme image or an ape illustration for a Lambo’s worth of cash were everywhere. “JPEG millionaires” became a thing. For those of us in tech, it was equal parts fascinating and bewildering: imagine telling a senior engineer a decade ago that digital monkey pictures would be a serious asset class – they’d think you’re utterly mad. Yet, for a brief moment, it really happened.

- It all ran like clockwork – This phrase captures the feeling in that peak hype period: everything just worked (financially, at least). Startups kept raising money at higher and higher values, NFT prices kept going up, and the usual skeptics or calls for caution were drowned out by the sheer momentum of the market. In the meme’s universe, this was a finely oiled machine: founders built ambitious moonshot plans, VCs kept funding them, token prices kept climbing, and everyone involved felt like a genius. It was almost boring how reliably things went up. Memes like “number go up” and “to the moon 🚀” – once jokey phrases – started to feel like actual business strategies.

So why is all of this framed as an angry rant? Because by 2023, we all witnessed that dream state implode. The meme is essentially the defeated voice of someone from the startup world raging at how quickly it all collapsed. The tone is sarcastic and hyperbolic on purpose. It’s poking fun at the founder angst and shock that came when the conditions changed seemingly overnight. One month you’re at a hackathon launching a quirky NFT marketplace convinced it’ll make you rich, and VC money is raining down. The next month, interest rates are hiked, and suddenly nobody wants to fund gimmicky ideas anymore. That shift was jarring – a genuine valuation whiplash. Many startups that raised at soaring valuations in 2021 had to confront 2022 with a sober reality: either you cut costs and try to actually make money, or you might not survive. Downrounds (raising new funding at a lower valuation than before, a big oops in startup-land) became common, and high-flying teams had to do layoffs to conserve cash. All those metrics that were forever climbing? They leveled off or nosedived. NFT trading volumes plummeted by ~90%+; prices for those once-hot JPEGs tanked (the same ape someone bought for $2.5M might fetch $100k or less now, if they’re lucky).

The humor here is that everyone knew on some level this was a bubble, but it was fun (and profitable) while it lasted. The meme exaggerates the nostalgic outrage of someone who wishes that bubble could have just kept expanding. The phrase “we had everything we needed” is comic because, in hindsight, those needs were totally unsustainable things: essentially free money and collective delusion. It’s like complaining that reality ruined your perfectly good fantasy. Senior devs laugh because they’ve seen hype cycles before and know the pattern: TechHypeCycle 101 – initial innovation, massive hype and investment, then the bubble bursts and a sobering bust follows. This cycle happened with the dot-com boom in the late ’90s (everyone added “.com” to their company name and saw stock valuations soar, until it crashed in 2000), and it just happened again with crypto/web3 startups and NFTs.

The choice of the Breaking Bad confrontation image is spot-on as a metaphor. In that scene, Mike is the grizzled veteran (think of him as the seasoned VC or the old engineer) scolding Walt (the overenthusiastic, prideful founder or perhaps the Fed chair). Mike lists all the advantages they had and basically says “you blew it up!” Similarly, the meme’s narrator is saying: we had the perfect setup in the startup world – why’d it have to end? The unspoken joke is: of course it had to end; it was built on zero-percent interest and speculative mania – but the dramatic blame still gets placed on some “stupid son of a b****” who ruined it. Many in tech wryly blame the Federal Reserve (Jerome Powell became a sort of meme villain for raising rates, with jokes like “Jerome pulled the plug on our party”). Others might blame reckless investors or scammy founders for popping the bubble. Either way, it’s funny because it externalizes the collapse in a very human way – we’re literally shooting the messenger (or the responsible adult) who turned off the music when the rave went on too long.

To engineers who went through this, there’s also a layer of coping humor. A lot of people’s projects and even jobs vanished when the funding dried up. You either laugh or cry, so you choose to laugh through a meme. For example, a startup engineer might recall how in 2021 their company rented swanky offices, hired like crazy, and gave out branded Patagonia vests – then in 2023 they’re suddenly told to tighten budgets and maybe find a path to profitability (gasp!). It’s a classic case of valuation whiplash: you’ve been thrown forward then violently backward, and you’re left with metaphorical neck pain. The meme compresses that whole saga into one spicy, cathartic quote. It’s effectively saying, “we had our fun, and now we’re left wandering the desert of reality, yelling about how great the party was.”

Technically inclined folks also chuckle at how blockchain hype and StartupCulture fads are encapsulated by “JPEGs that sold for millions” – it’s such a ridiculous highlight of that era. It’d be like summarizing the dot-com era by saying “we had sock puppet mascots raising $300 million IPOs” (a nod to Pets.com). It deliberately picks the most meme-able, slightly cringe aspect of the boom to emphasize how absurd things got. And yes, for a while, every startup’s metrics only pointed one way: user counts, GMV, token prices, valuation – all exponential curves heading upward. That’s the “ran like clockwork” part: a wry reference to those smooth, ever-growing charts in pitch decks and All Hands meetings. Of course, now we know those were bubble charts, not sustainable business indicators.

To illustrate how absurdly predictable (and precarious) the cycle was, here’s a tongue-in-cheek pseudo-code of the situation:

// Pseudocode for the tech boom cycle under zero interest

while (interestRate === 0) {

startup.valuation *= 2; // valuations double each funding round

nft.price = Math.random() * 10_000_000; // random JPEG gets a multi-million $ tag

}

// Now the punchline: interest rate rises and the party ends

if (interestRate > 0) {

throw new Error("Party's over: valuations crashed!"); // the bubble pops

}

In real life, that throw happened in 2022 when rates went up. The Error took the form of mass layoffs, down rounds, bankrupt crypto firms, and forlorn Slack channels with rocket emojis suddenly scrubbed away. The code comments capture it: as long as money was practically free (interestRate === 0), valuations kept looping higher and even silly assets like random NFTs fetched crazy prices. But once that condition failed, the whole loop broke disastrously.

Ultimately, the meme’s humor is in the dramatic irony. The speaker in the meme acts genuinely heartbroken that the TechHypeCycle ended, as if a great injustice occurred (“We had everything and you ruined it!”). Senior tech folks reading it know that this tongue-in-cheek anger is really directed at how fickle and absurd the boom was in the first place. It’s a bit of dark comedy: we’re mockingly mourning something we all secretly knew was unsustainable. It’s funny because the rant is over-the-top, yet every item in it rings true about that time. It’s both a roast and a eulogy for the age of free money and NFT utopia. And for anyone who endured the subsequent crash, the meme provides a moment to smirk and think, “Yep, that wild ride really happened – and thank goodness we can joke about it now.”

Level 4: Monetary Perpetual Motion

At the height of the tech boom, the financial conditions resembled a monetary perpetual motion machine – something theoretically too good to be true. Under a prolonged Zero Interest Rate Policy (ZIRP), the cost of money was effectively nil. This meant venture investors could borrow or allocate capital with almost no penalty for risk. In classical finance terms, the discount rate (the r used to discount future cash flows in valuation models) drifted toward zero, drastically inflating the present value of distant future gains. Mathematically, if we model a startup’s value as the present value of expected future profits:

$$ P_{0} = \frac{CF_{1}}{(1+r)} + \frac{CF_{2}}{(1+r)^2} + \cdots + \frac{CF_{T}}{(1+r)^T}, $$

as $r \to 0$, each term $\frac{1}{(1+r)^t} \to 1$. In the extreme case of $r = 0$, future earnings decades away count just as heavily as next year’s. The summation of many years of expected growth is barely diminished by discounting. If $T$ is large (or effectively infinite for a company assumed to thrive indefinitely) and we anticipate growth, the series can blow up. In simpler terms, when $r$ is near 0, the formula outputs grotesquely large $P_{0}$ values – valuations skyrocketed. This is why in a zero-rate environment, even companies with profits far off on the horizon (or none at all yet) could command enormous valuations. With capital essentially free, any promising startup could raise money at a high price, because the opportunity cost of investing was so low. Money chasing the next big tech idea had almost no gravity pulling it down.

This manifested as an apparent defiance of economic gravity – a bubble driven by fundamentals turned on their head. It was akin to discovering an infinite energy cheat code in the economy: if money costs nothing, you can keep pouring fuel into risky ventures without immediate consequence. Startups could burn cash to grab market share and worry about profits later, while investors saw sky-high paper returns on the assumption that future gains would justify it. The entire ecosystem functioned like a finely-tuned closed system – a finance version of a perpetual motion machine – where one input (nearly free capital) kept everything spinning upwards. Of course, in physics and finance alike, perpetual motion is illusory; eventually entropy (or economic reality) intervenes.

In parallel, NFT technology (Non-Fungible Tokens on the blockchain) provided a novel platform for speculation. NFTs are underpinned by cryptographic and distributed systems principles: a token like an ERC-721 on Ethereum can represent unique ownership of a digital asset. Technically, an NFT is just a unique ledger entry pointing to some metadata (often a URL of a JPEG image). The innovation was digital scarcity: guaranteeing one true owner of a digital item via blockchain consensus. In theory, this was a legitimate breakthrough for provenance in art and collectibles. But under ZIRP conditions, that technical breakthrough was turbocharged into a speculative mania. People flush with liquidity started trading JPEGs as if they were million-dollar assets. Why? Because in an environment where every risk asset was soaring, even a crypto token for a cartoon ape or pixelated punk could be rationalized as valuable – either as the next big social status symbol or simply because everyone believed they could later sell it for more (the classic greater fool theory of bubbles).

It’s key to note how tightly coupled this frenzy was to the macro environment. The venture funding glut and NFT bubble were not random; they were an emergent property of near-zero interest rates. Academic papers and economic history tell us that prolonged periods of cheap money encourage asset bubbles – from tulip bulbs in the 17th century to housing in the 2000s. The tech sector in the late 2010s–2021 was simply the latest domain to experience this, fueled by unprecedented global liquidity. Startups assumed an infinite runway (just raise the next round when you need cash) and investors valued growth over everything (even basic financial sanity) because the risk-free rate was effectively nonexistent. In engineering terms, the usual damping factor in the system had been removed, leading to runaway feedback. Every success story (or even rumor of success) attracted more capital, which created more success stories on paper – a positive feedback loop reminiscent of a self-sustaining reaction. It all felt very clockwork: predictable growth, round after round, unicorn after unicorn minted, token after token soaring in price.

However, just as perpetual motion violates physical laws (friction and energy conservation will catch up), the free money machine violated economic sustainability. The shift came when inflation, an inevitable side-effect of excess liquidity, reared its head and central banks slammed the brakes. In late 2021 and through 2022, the U.S. Federal Reserve and other central banks began a macroeconomic regime shift, hiking interest rates rapidly to around 4-5%. This was the equivalent of reintroducing friction into the system. The discount rate $r$ in those valuation equations didn’t just tick up slowly — it spiked. Even a few percentage points of real cost of capital are like throwing sand in the gears of that clockwork funding machine. The result was mathematically predictable: when $r$ moves from ~0% to ~5%, the same projected cash flows yield a dramatically lower $P_{0}$. Valuations for high-growth tech companies contracted almost overnight, a harsh demonstration of how sensitive those sky-high valuations were to the zero-rate assumption. What had seemed like invincible “up-and-to-the-right” charts suddenly looked like over-inflated balloons meeting a pin.

In summary, the meme laments a fleeting era that appeared to defy the normal laws of finance. It highlights the fundamental truth that neither energy nor money can be free forever without consequences. The post-2021 tech downturn was essentially economic gravity pulling those lofty valuations and million-dollar JPEGs back to Earth. The humor at this level is cerebral: it’s recognizing the almost absurd theoretical underpinnings of that wild ride — how an entire startup ecosystem bet on an indefinite monetary anomaly, and how inevitability caught up with it. Just as engineers know a perpetual motion machine can’t run indefinitely, investors and senior engineers (perhaps grudgingly) knew ZIRP couldn’t last forever either. The meme’s dramatic phrasing, in this light, becomes a tongue-in-cheek ode to a violated impossibility: if only we could have kept that free money machine running like clockwork! But reality, like physics, always wins.

Description

The image is a screenshot of a tweet from the account "Dr. Parik Patel, BA, CFA, ACCA Esq. @ParikPatelCFA". The tweet text reads: “We had a good thing you stupid son of a bitch. We had zero rates. We had unlimited startup funding. We had soaring valuations. We had JPEGs that sold for millions. We had everything we needed and it all ran like clockwork.” Below the tweet is a still from Breaking Bad where two bald characters (faces blurred) confront each other in a desert setting, underscoring the intensity of the rant. Technically, the meme riffs on the post-ZIRP macro shift: cheap capital, hyper-growth valuations, and the NFT frenzy that once fueled infinite runway for startups, all now gone. Senior engineers will recognise the sarcastic lament for an era when VC money flowed freely, JPEGs masqueraded as assets, and every metrics dashboard pointed “up-and-to-the-right.”

Comments

12Comment deleted

Remember when our risk model was literally `money.free()? true : pivotToAI();` - turns out that branch just hit production

The only thing more volatile than our microservices in production was watching our Series B valuation evaporate faster than a Redis cache after someone forgot to configure persistence - turns out 'move fast and break things' also applied to the Fed's monetary policy

Ah yes, the ZIRP era - when your Series A pitch deck could literally be a JPEG of a monkey, your burn rate was a feature not a bug, and 'path to profitability' was just a theoretical CS problem you'd solve eventually. Now we're all debugging our cap tables in production while the Fed's interest rate hikes are throwing unhandled exceptions across the entire startup ecosystem. Turns out 'move fast and break things' works great until the things breaking are your runway calculations and the 'fast' part is how quickly investors ghost your emails

We hard‑coded ZIRP as a global singleton; when the Fed shipped a breaking‑change release, every valuation microservice started throwing 500s and the JPEG service dropped to 0 QPS

Peak blockchain scalability: mint infinite JPEGs on one chain, dump liquidity across all others

Someone toggled off the global ZeroInterestRates feature flag and half the stack threw NullCapitalException - turns out our ‘scale’ was just DependencyInjection(VentureCapital)

Calling in the explanation squad! Explanation squad, come in! Over. Comment deleted

Also those images what were they really? Bitmaps or vector graphics or jpegs? Like the ones I saw had no obvious compression artifacts at a first glance. Comment deleted

It doesn’t touch topic of any issues with jpegs. Instead, it’s just a common word to describe any kind of picture "on blockchain" Comment deleted

Yes I understood but my question was wether on the blockchain where you can basically store binary data, how it was used. Like real bitmap or PNG or JPG? Comment deleted

Nah, no one stores images on blockchain for real. Existing solution only store hash or alike data so those who actually store able to generate proof of store Comment deleted

Ahhh got it thanks Comment deleted