Historical Irony: Egypt Expresses Concerns Over New Pyramid Schemes

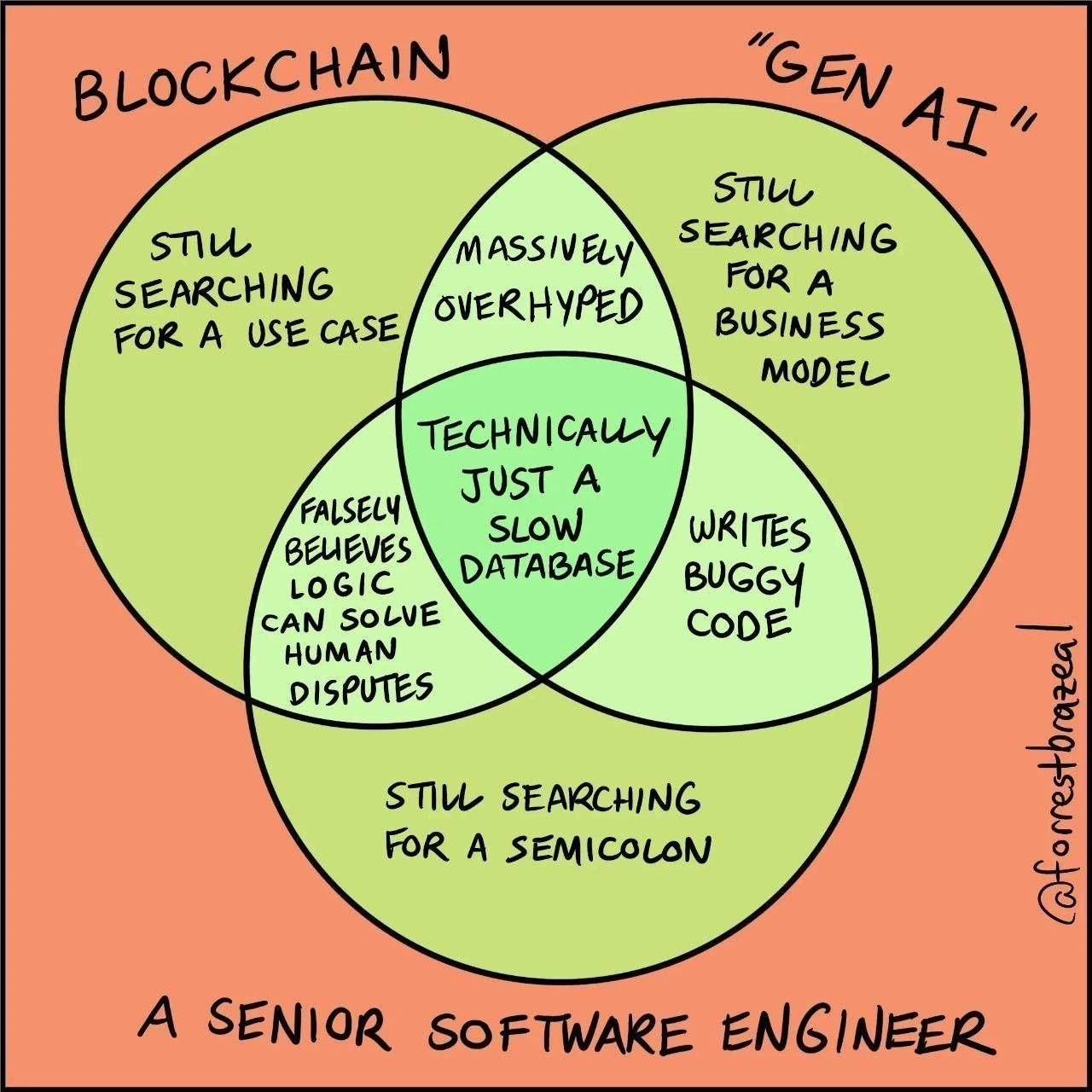

Why is this Blockchain meme funny?

Level 1: Not That Pyramid

Imagine your class loves building huge pyramids out of LEGO blocks. It’s a fun project and everyone is proud of the big pyramid you built together. But then someone starts a sneaky pyramid game at school: the first kid to join gets a bunch of candy from kids who join later. Those new kids are promised they’ll get candy too, but only if even more kids join after them. Eventually, the game runs out of new players and the last kids end up with no candy at all (they feel cheated and sad). Of course, the teacher would quickly step in and ban this game because it’s unfair and people are getting hurt. Now, if a student joked, “I thought this school liked pyramids!”, they’re being silly by mixing up the two ideas of a pyramid. Just because everyone likes the real pyramid you built (the fun, honest kind) doesn’t mean they’ll accept a pyramid scam that tricks people. That’s exactly the point of the meme: Egypt loves its real pyramids, but it isn’t okay with a pyramid-shaped money scam that could hurt people.

Level 2: Is Crypto a Pyramid Scheme?

This meme jokes that Egypt loves pyramids (the huge ancient stone monuments), yet it banned cryptocurrency – implying some folks think crypto is basically a pyramid scheme. In other words, it’s a play on the word “pyramid”: Egypt is famous for real pyramids, but a “pyramid scheme” is something very different (and not good). In fact, Egypt’s central bank did issue a ban on creating or dealing in cryptocurrency around 2022.

First off, what is a cryptocurrency? It’s a form of digital money (for example, Bitcoin or Ethereum) that isn’t controlled by any government or central bank. Instead of relying on a bank’s ledger, transactions are verified by a network of computers using blockchain technology. A blockchain is basically a shared public ledger (like a digital record book) that is maintained by many computers at once. Every time transactions happen, they get grouped into a “block” and added to the chain of earlier blocks. This chain is secured by cryptography, making it nearly impossible to alter past records. Because of this tech, cryptocurrencies can operate in a decentralized way (no single authority in charge).

These kinds of innovations are part of FinTech (short for financial technology) – new tech that shakes up or improves traditional finance. In the late 2010s and early 2020s, crypto became a huge craze. Prices of popular cryptocurrencies like Bitcoin shot up dramatically, and tons of new coins and projects appeared. There was a lot of excitement (and hype) around blockchain and crypto. Many people were investing, hoping to get rich quickly or at least not miss out on the next big thing (FOMO – “fear of missing out” – was a real factor).

Now, a central bank is the national authority that manages a country’s money and financial rules. For example, Egypt’s central bank controls the supply of the Egyptian pound (their currency), sets interest rates, and oversees banks to keep the economy stable. Central banks generally don’t like things that could destabilize the financial system or hurt consumers. So from their point of view, cryptocurrency looked risky and troublesome. Why? Here are a few reasons:

- No safety net – If people lose money due to a crypto scam or a price crash, there’s no bank insurance or government protection to help them recover their losses.

- Crime risks – Cryptocurrencies can be used somewhat anonymously and across borders. Regulators worry they could enable money laundering, fraud, or other illegal activities without detection.

- Losing control – If everyone started using Bitcoin or digital coins instead of the official currency, the central bank would struggle to manage the money supply and economic stability. It would be much harder for them to monitor what’s happening in the economy or to control things like inflation.

Because of concerns like these, Egypt’s central bank decided to outlaw unregulated crypto. Essentially, they didn’t want digital money circulating outside of the official system. The headline in the meme is highlighting that rule: Egypt prohibited issuing new cryptocurrencies or promoting activities related to them.

Now, what exactly is a pyramid scheme? It’s a fraudulent money-making setup where the main way people make money is by recruiting new participants, rather than by any real business activity. The structure looks like a pyramid: you (at the top) recruit, say, 5 people beneath you; those 5 each recruit their own group of new people, and so on. Each new tier of people pays money that flows up the pyramid to those above. As the scheme grows, it needs an ever-increasing number of new recruits (forming a wider and wider base) to keep money flowing upward. Inevitably, it becomes impossible to sustain — eventually you run out of new people to recruit, and the whole pyramid collapses. When it collapses, the most recent recruits (at the bottom of the pyramid) lose their money, while the folks at the top might have already profited. Importantly, there’s no genuine product or investment in a pyramid scheme; it’s all about moving money from later recruits to earlier recruits. (A Ponzi scheme is a very similar idea — basically one person at the top paying early investors with money from later investors. Both are illegal scams that enrich a few and hurt many.)

Some critics say certain cryptocurrency projects resemble pyramid schemes. Why? Imagine a new coin that doesn’t have much practical use, but its price keeps rising mainly because more and more people are buying in, hoping for quick gains. Early adopters (and especially the creators) hype it up, and as long as lots of new buyers keep entering the market, the price stays high — allowing those early folks to sell and make a big profit. But if the hype dies down or new investors stop coming, the price can crash, leaving the latecomers holding the bag (stuck with losses). In this way, an overhyped crypto coin can feel like a pyramid scheme: it relies on an expanding base of new money to pay off the initial investors. There have been real cases where crypto ventures worked like this — they raised money from the public, paid old investors with new investors’ funds to show “profits” for a while, and then collapsed once no new money came in. That’s essentially a Ponzi scheme with a crypto twist.

So, the tweet saying “I thought Egypt liked pyramids” is a tongue-in-cheek quip. It’s mixing up the two meanings of pyramid in a jokey way. Egypt loves its real pyramids (the ancient wonders of the world), but that doesn’t mean it’s okay with pyramid schemes. The person tweeting is pretending to be “confused” that Egypt would ban crypto if it has the word pyramid associated with it. Of course, Egypt’s love of actual pyramids has nothing to do with banning a pyramid-shaped money scam. The meme is pointing out, in a funny way, that a cutting-edge trend like crypto can sometimes be just a rehash of an old scam — and even the land of the pyramids isn’t falling for it.

Level 3: Crypto in De Nile

"Wtf I thought Egypt liked pyramids."

Barely Sociable’s tweet sets a cheeky tone with a pun: since Egypt is famous for actual pyramids, the poster jokingly wonders why the country’s officials aren’t fans of these new “pyramid” schemes (cryptocurrencies). The meme image pairs this tweet with a serious headline from Egypt Today — essentially Egypt’s central bank is banning the creation or trade of cryptocurrencies outright. The humor comes from the contrast and wordplay: Egypt loves its literal pyramids, but clearly not the metaphorical kind (financial pyramid schemes).

This meme is a piece of tech humor – a bit of industry satire highlighting the tension between flashy FinTech innovation and the reality of a regulatory clampdown. A country known for enduring monuments (the Pyramids of Giza) is cracking down on ephemeral digital assets that skeptics liken to modern pyramid schemes. For seasoned tech observers, the joke lands because they've seen cryptocurrency mania soar high and then crash headfirst into the brick wall of government regulation. After the wild speculative bubble of 2021, countries worldwide (Egypt included) started pumping the brakes on unregulated crypto trading by early 2022.

Egypt's central bank (like many regulators) is not amused by unregulated digital currencies threatening their control of the money system. If people switch to a private cryptocurrency, it bypasses traditional banking safeguards and can turn finance into a Wild West free-for-all. In a nutshell, their concerns include:

- Investor protection – If naive investors lose big money to volatile or scammy coins, there’s no safety net (and they might blame the authorities afterward).

- Financial crime – Untracked crypto transactions can enable money laundering or fund illegal activities outside the law’s reach.

- Monetary control – If everyone used Bitcoin or other crypto instead of the Egyptian Pound, the central bank would lose control over the money supply, inflation, and overall economic stability.

So from the regulator’s perspective, banning crypto is about preventing what they see as a pyramid-style scam from becoming a national problem. There's a rich irony here that veteran techies appreciate: the blockchain world promised to build trust with math and code, yet it ended up rekindling some of the oldest financial scams in history. And fittingly, the country famous for literal pyramids is calling out these modern digital "pyramids" for what they are.

The meme wouldn’t be as funny if there weren’t a grain of truth to it. Plenty of cryptocurrency projects have turned out to be outright Ponzi schemes or multi-level marketing hustles wearing a high-tech facade. Tech veterans still cringe remembering cases like BitConnect, which famously collapsed once people realized its “guaranteed” returns were a sham. It’s the same old con, just rebranded with buzzwords and blockchain.

Interestingly, even the process of building a blockchain (through cryptocurrency mining) gobbles up tremendous resources — not entirely unlike how Pharaohs marshaled massive manpower to erect the pyramids of Giza. Bitcoin miners worldwide expend colossal amounts of electricity solving cryptographic puzzles to secure the ledger. The Pharaohs expended countless labor hours hauling stone blocks into a giant tomb. Both are monumental undertakings, but at least the real pyramids have stood solid for millennia, whereas a flimsy crypto pyramid scheme can crumble in months.

Those who’ve been around the tech block can’t help but chuckle at this meme because it nails a fundamental truth: Egypt is totally fine with pyramids that stand the test of time, but not so fine with get-rich-quick pyramid schemes built on hype. In essence, the joke cleverly captures how even in cutting-edge tech we end up reinventing age-old problems – and how regulators (with perfect irony) step in to remind everyone of that fact.

Description

The image is a composite of two screenshots. The top part is a tweet from the user 'Barely Sociable' which reads, 'Wtf I thought Egypt liked pyramids'. Below it is a screenshot of a news headline from 'egypt today' that states, 'Egypt's central bank prohibits issuing cryptocurrencies or carrying out activities related to them'. The humor is a sophisticated pun, playing on the dual meaning of 'pyramid'. It juxtaposes Egypt, a country famous for its ancient architectural pyramids, with the modern pejorative term 'pyramid scheme,' which is frequently used by critics to describe the structure and speculative nature of many cryptocurrency projects. The tweet feigns confusion, creating a witty and ironic commentary on the perceived legitimacy and stability of the cryptocurrency market

Comments

10Comment deleted

Egypt has 5,000 years of technical debt from their last pyramid projects; they're not about to take on a new, decentralized one with no project manager

After 45 centuries maintaining the world’s only stateful monolith that’s still up, Egypt isn’t impressed by your sharded, proof-of-greater-fool pyramid protocol

After 4,500 years of perfecting distributed architecture with redundant stone blocks, Egypt's central bank decides the blockchain's consensus mechanism isn't Byzantine fault-tolerant enough for their taste

Egypt's pyramids have 4500 years of uptime with zero rug pulls - a Lindy benchmark no L1 chain has survived a single bear market against

When you realize Egypt's central bank isn't banning the data structure with O(log n) operations, but rather the financial instruments with O(∞) promises and O(0) actual value. At least the ancient pyramids had better uptime than most crypto exchanges

Egypt's central bank just issued the ultimate breaking change: deprecated all cryptocurrencies

First compliance rule I’ve seen that bans a consensus algorithm: no PoW, no PoS, and definitely no PoNZI

Egypt bans crypto - guess they prefer pyramids with literal blocks and millennia-grade finality, not the tokenomics kind where consensus is just your referral graph

Fun fact the first country to ban Bitcoins is USA and now the most Bitcoin owner is also USA. Comment deleted

Fun fact, you can't know where bitcoins are, that's the point, it's only a point in the sky Comment deleted